"/><stop offset="1" stop-color="rgb(3, 73, 122)"/></linearGradient><linearGradient id="qyqFJaVjA-1921182794-linear-gradient" x1="0" x2="1" y1="0.5558218829289385" y2="0.4441781170710614"><stop offset="0" stop-color="rgb(29, 170, 88)"/><stop offset="1" stop-color="rgb(0, 143, 203)"/></linearGradient><linearGradient id="KBptSRBQO-1921182794-linear-gradient" x1="0" x2="1" y1="0.5556785500517466" y2="0.44432144994825334"><stop offset="0" stop-color="rgb(29, 170, 88)"/><stop offset="1" stop-color="rgb(0, 143, 203)"/></linearGradient><linearGradient id="Kgw6PgukY-1921182794-linear-gradient" x1="0.2117440484028747" x2="0.7882559515971252" y1="1" y2="5.551115123125783e-17"><stop offset="0" stop-color="rgb(0, 143, 203)"/><stop offset="1" stop-color="rgb(255, 255, 255)"/></linearGradient></defs><g d="M 25.388 5.232 L 25.388 10.89 L 26.819 10.89 C 29.017 10.89 30.33 9.837 30.33 8.061 C 30.33 6.285 28.996 5.232 26.766 5.232 L 25.387 5.232 Z M 24 12.008 L 24 4.118 L 26.79 4.118 C 29.895 4.118 31.746 5.599 31.746 8.065 C 31.746 10.53 29.916 12.012 26.844 12.012 L 24 12.012 Z M 38.74 9.415 C 38.233 8.438 37.652 7.265 37.166 6.248 C 36.665 7.317 36.137 8.373 35.582 9.415 Z M 37.113 4 L 37.22 4 L 41.53 12.015 L 40.064 12.015 L 39.179 10.413 L 35.129 10.413 L 34.266 12.015 L 32.799 12.015 L 37.109 4 Z M 45.954 5.232 L 45.954 12.008 L 44.567 12.008 L 44.567 5.232 L 41.809 5.232 L 41.809 4.118 L 48.714 4.118 L 48.714 5.232 L 45.955 5.232 Z M 54.927 9.415 C 54.421 8.438 53.84 7.265 53.354 6.248 C 52.853 7.317 52.324 8.373 51.77 9.415 L 54.928 9.415 Z M 53.302 4 L 53.409 4 L 57.719 12.015 L 56.256 12.015 L 55.371 10.413 L 51.321 10.413 L 50.458 12.015 L 48.992 12.015 Z M 59.88 12.008 L 59.88 4.114 L 61.268 4.114 L 61.268 10.89 L 65.158 10.89 L 65.158 12.008 Z M 68.892 4.5 L 67.5 4.5 L 67.5 12.39 L 68.892 12.39 Z M 76.924 12.177 C 73.994 12.177 72 10.522 72 8.089 C 72 5.656 74.002 4 76.935 4 C 78.326 4 79.208 4.305 79.779 4.57 L 79.779 5.808 C 78.894 5.415 77.935 5.214 76.967 5.217 C 74.844 5.217 73.403 6.379 73.403 8.089 C 73.403 9.799 74.826 10.972 76.924 10.972 C 77.495 10.972 78.216 10.874 78.658 10.732 L 78.658 8.408 L 79.993 8.408 L 79.993 11.578 C 79.218 11.942 77.97 12.181 76.924 12.181 M 85.16 7.698 C 84.792 7.368 84.385 7.03 84.157 6.808 C 84.157 7.106 84.167 7.586 84.167 7.905 L 84.167 12.038 L 82.791 12.038 L 82.791 4.024 L 82.888 4.024 L 87.844 8.475 L 88.836 9.376 C 88.825 9.071 88.825 8.664 88.825 8.279 L 88.825 4.147 L 90.201 4.147 L 90.201 12.161 L 90.116 12.161 L 85.159 7.698 Z M 42 17.859 L 43.799 14.508 L 43.941 14.508 L 45.743 17.859 L 44.98 17.859 L 44.627 17.224 L 43.107 17.224 L 42.764 17.859 Z M 44.366 16.661 C 44.198 16.331 44.034 16 43.874 15.666 C 43.72 15.993 43.542 16.346 43.378 16.661 Z M 47.799 14.555 C 49.09 14.555 49.85 15.18 49.85 16.207 C 49.85 17.235 49.097 17.859 47.82 17.859 L 46.607 17.859 L 46.607 14.555 Z M 47.32 15.161 L 47.32 17.249 L 47.81 17.249 C 48.63 17.249 49.13 16.868 49.13 16.204 C 49.13 15.539 48.623 15.158 47.791 15.158 L 47.321 15.158 L 47.321 15.161 Z M 52.07 17.907 L 52.087 17.874 L 50.307 14.554 L 51.085 14.554 L 51.795 15.913 C 51.941 16.2 52.059 16.425 52.177 16.672 C 52.341 16.327 52.527 15.986 52.751 15.553 L 53.271 14.558 L 54.05 14.558 L 52.251 17.91 L 52.07 17.91 Z M 55.584 17.859 L 54.87 17.859 L 54.87 14.555 L 55.584 14.555 Z M 56.804 17.739 L 56.726 17.71 L 56.726 17.02 L 56.836 17.068 C 57.146 17.198 57.536 17.286 57.86 17.286 C 58.082 17.286 58.26 17.253 58.381 17.195 C 58.478 17.144 58.535 17.079 58.535 16.988 C 58.535 16.886 58.495 16.81 58.395 16.741 C 58.278 16.657 58.085 16.585 57.793 16.498 C 57.029 16.276 56.697 15.996 56.697 15.459 C 56.697 14.875 57.193 14.5 58.028 14.5 C 58.363 14.5 58.724 14.562 58.984 14.668 L 59.034 14.686 L 59.034 15.357 L 58.924 15.307 C 58.648 15.188 58.35 15.126 58.049 15.125 C 57.839 15.125 57.668 15.155 57.55 15.219 C 57.454 15.27 57.396 15.343 57.396 15.437 C 57.396 15.528 57.436 15.601 57.532 15.673 C 57.65 15.761 57.839 15.84 58.128 15.928 C 58.884 16.156 59.234 16.425 59.234 16.951 C 59.234 17.551 58.742 17.914 57.882 17.914 C 57.514 17.914 57.104 17.844 56.801 17.736 Z M 62.089 14.5 C 63.273 14.5 64.076 15.198 64.076 16.21 C 64.076 17.224 63.27 17.921 62.089 17.921 C 60.908 17.921 60.101 17.224 60.101 16.211 C 60.101 15.198 60.907 14.501 62.088 14.501 Z M 62.089 17.271 C 62.834 17.271 63.352 16.846 63.352 16.211 C 63.352 15.575 62.834 15.147 62.088 15.147 C 61.343 15.147 60.818 15.572 60.818 16.211 C 60.818 16.85 61.339 17.271 62.088 17.271 Z M 66.499 14.558 C 67.373 14.558 67.908 14.954 67.908 15.63 C 67.908 16.073 67.64 16.41 67.188 16.567 L 68.043 17.863 L 67.255 17.863 L 66.505 16.683 L 65.906 16.683 L 65.906 17.863 L 65.2 17.863 L 65.2 14.559 L 66.499 14.559 Z M 65.906 15.165 L 65.906 16.098 L 66.527 16.098 C 66.93 16.098 67.194 15.938 67.194 15.63 C 67.194 15.321 66.924 15.165 66.502 15.165 Z M 69.325 14.591 L 70.263 15.935 L 71.23 14.558 L 72.047 14.558 L 70.62 16.574 L 70.62 17.863 L 69.906 17.863 L 69.906 16.573 L 68.479 14.559 L 69.296 14.559 L 69.321 14.591 Z M 2.034 14.412 L 9.998 14.325 L 11.532 11.558 L 13.58 15.168 L 1.602 15.168 L 1.032 16.17 L 15.285 16.17 L 12.092 10.541 L 12.549 9.717 L 16.673 16.987 L 0.571 16.987 L 0 17.989 L 18.386 17.989 L 13.116 8.7 L 13.559 7.902 L 19.285 18 L 20.42 18 L 10.212 0 Z M 10.212 2.004 L 12.984 6.896 L 12.542 7.695 L 10.305 3.755 L 4.799 13.381 L 3.75 13.392 Z M 10.305 5.752 L 11.981 8.708 L 11.525 9.532 L 10.319 7.408 L 7.139 13.352 L 5.951 13.367 Z M 10.347 9.459 L 10.965 10.545 L 9.423 13.323 L 8.271 13.337 Z M 0 18.002 L 0.57 17 L 16.677 17 L 18.387 18.003 L 0 18.003 Z M 1 16.006 L 1.567 15 L 13.545 15 L 15.254 16.006 Z M 10.078 14.29 L 14.406 6.52 L 13.825 5.5 L 9.5 13.292 Z" fill="transparent" height="18.003px" id="K_8etyHP8" width="90.20100036621093px"><path d="M 1.388 1.232 L 1.388 6.89 L 2.819 6.89 C 5.017 6.89 6.33 5.837 6.33 4.061 C 6.33 2.285 4.996 1.232 2.766 1.232 L 1.387 1.232 Z M 0 8.008 L 0 0.118 L 2.79 0.118 C 5.895 0.118 7.746 1.599 7.746 4.065 C 7.746 6.53 5.916 8.012 2.844 8.012 L 0 8.012 Z M 14.74 5.415 C 14.233 4.438 13.652 3.265 13.166 2.248 C 12.665 3.317 12.137 4.373 11.582 5.415 Z M 13.113 0 L 13.22 0 L 17.53 8.015 L 16.064 8.015 L 15.179 6.413 L 11.129 6.413 L 10.266 8.015 L 8.799 8.015 L 13.109 0 Z M 21.954 1.232 L 21.954 8.008 L 20.567 8.008 L 20.567 1.232 L 17.809 1.232 L 17.809 0.118 L 24.714 0.118 L 24.714 1.232 L 21.955 1.232 Z M 30.927 5.415 C 30.421 4.438 29.84 3.265 29.354 2.248 C 28.853 3.317 28.324 4.373 27.77 5.415 L 30.928 5.415 Z M 29.302 0 L 29.409 0 L 33.719 8.015 L 32.256 8.015 L 31.371 6.413 L 27.321 6.413 L 26.458 8.015 L 24.992 8.015 Z M 35.88 8.008 L 35.88 0.114 L 37.268 0.114 L 37.268 6.89 L 41.158 6.89 L 41.158 8.008 Z" fill="rgb(132, 130, 142)" height="8.015px" id="jAL5eYCXu" transform="translate(24 4)" width="41.15800106811523px"/><path d="M 1.392 0 L 0 0 L 0 7.89 L 1.392 7.89 Z" fill="rgb(132, 130, 142)" height="7.890000000000001px" id="u8cKeOXNI" transform="translate(67.5 4.5)" width="1.391999999999996px"/><path d="M 4.924 8.177 C 1.994 8.177 0 6.522 0 4.089 C 0 1.656 2.002 0 4.935 0 C 6.326 0 7.208 0.305 7.779 0.57 L 7.779 1.808 C 6.894 1.415 5.935 1.214 4.967 1.217 C 2.844 1.217 1.403 2.379 1.403 4.089 C 1.403 5.799 2.826 6.972 4.924 6.972 C 5.495 6.972 6.216 6.874 6.658 6.732 L 6.658 4.408 L 7.993 4.408 L 7.993 7.578 C 7.218 7.942 5.97 8.181 4.924 8.181 M 13.16 3.698 C 12.792 3.368 12.385 3.03 12.157 2.808 C 12.157 3.106 12.167 3.586 12.167 3.905 L 12.167 8.038 L 10.791 8.038 L 10.791 0.024 L 10.888 0.024 L 15.844 4.475 L 16.836 5.376 C 16.825 5.071 16.825 4.664 16.825 4.279 L 16.825 0.147 L 18.201 0.147 L 18.201 8.161 L 18.116 8.161 L 13.159 3.698 Z" fill="rgb(132, 130, 142)" height="8.181px" id="kN7yl8Gfy" transform="translate(72 4)" width="18.201000366210934px"/><path d="M 0 3.359 L 1.799 0.008 L 1.941 0.008 L 3.743 3.359 L 2.98 3.359 L 2.627 2.724 L 1.107 2.724 L 0.764 3.359 Z M 2.366 2.161 C 2.198 1.831 2.034 1.5 1.874 1.166 C 1.72 1.493 1.542 1.846 1.378 2.161 Z M 5.799 0.055 C 7.09 0.055 7.85 0.68 7.85 1.707 C 7.85 2.735 7.097 3.359 5.82 3.359 L 4.607 3.359 L 4.607 0.055 Z M 5.32 0.661 L 5.32 2.749 L 5.81 2.749 C 6.63 2.749 7.13 2.368 7.13 1.704 C 7.13 1.039 6.623 0.658 5.791 0.658 L 5.321 0.658 L 5.321 0.661 Z M 10.07 3.407 L 10.087 3.374 L 8.307 0.054 L 9.085 0.054 L 9.795 1.413 C 9.941 1.7 10.059 1.925 10.177 2.172 C 10.341 1.827 10.527 1.486 10.751 1.053 L 11.271 0.058 L 12.05 0.058 L 10.251 3.41 L 10.07 3.41 Z M 13.584 3.359 L 12.87 3.359 L 12.87 0.055 L 13.584 0.055 Z M 14.804 3.239 L 14.726 3.21 L 14.726 2.52 L 14.836 2.568 C 15.146 2.698 15.536 2.786 15.86 2.786 C 16.082 2.786 16.26 2.753 16.381 2.695 C 16.478 2.644 16.535 2.579 16.535 2.488 C 16.535 2.386 16.495 2.31 16.395 2.241 C 16.278 2.157 16.085 2.085 15.793 1.998 C 15.029 1.776 14.697 1.496 14.697 0.959 C 14.697 0.375 15.193 0 16.028 0 C 16.363 0 16.724 0.062 16.984 0.168 L 17.034 0.186 L 17.034 0.857 L 16.924 0.807 C 16.648 0.688 16.35 0.626 16.049 0.625 C 15.839 0.625 15.668 0.655 15.55 0.719 C 15.454 0.77 15.396 0.843 15.396 0.937 C 15.396 1.028 15.436 1.101 15.532 1.173 C 15.65 1.261 15.839 1.34 16.128 1.428 C 16.884 1.656 17.234 1.925 17.234 2.451 C 17.234 3.051 16.742 3.414 15.882 3.414 C 15.514 3.414 15.104 3.344 14.801 3.236 Z M 20.089 0 C 21.273 0 22.076 0.698 22.076 1.71 C 22.076 2.724 21.27 3.421 20.089 3.421 C 18.908 3.421 18.101 2.724 18.101 1.711 C 18.101 0.698 18.907 0.001 20.088 0.001 Z M 20.089 2.771 C 20.834 2.771 21.352 2.346 21.352 1.711 C 21.352 1.075 20.834 0.647 20.088 0.647 C 19.343 0.647 18.818 1.072 18.818 1.711 C 18.818 2.35 19.339 2.771 20.088 2.771 Z M 24.499 0.058 C 25.373 0.058 25.908 0.454 25.908 1.13 C 25.908 1.573 25.64 1.91 25.188 2.067 L 26.043 3.363 L 25.255 3.363 L 24.505 2.183 L 23.906 2.183 L 23.906 3.363 L 23.2 3.363 L 23.2 0.059 L 24.499 0.059 Z M 23.906 0.665 L 23.906 1.598 L 24.527 1.598 C 24.93 1.598 25.194 1.438 25.194 1.13 C 25.194 0.821 24.924 0.665 24.502 0.665 Z M 27.325 0.091 L 28.263 1.435 L 29.23 0.058 L 30.047 0.058 L 28.62 2.074 L 28.62 3.363 L 27.906 3.363 L 27.906 2.073 L 26.479 0.059 L 27.296 0.059 L 27.321 0.091 Z" fill="rgb(142, 140, 153)" height="3.421000000000001px" id="P22Fbj16y" transform="translate(42 14.5)" width="30.047000091552746px"/><path d="M 2.034 14.412 L 9.998 14.325 L 11.532 11.558 L 13.58 15.168 L 1.602 15.168 L 1.032 16.17 L 15.285 16.17 L 12.092 10.541 L 12.549 9.717 L 16.673 16.987 L 0.571 16.987 L 0 17.989 L 18.386 17.989 L 13.116 8.7 L 13.559 7.902 L 19.285 18 L 20.42 18 L 10.212 0 Z M 10.212 2.004 L 12.984 6.896 L 12.542 7.695 L 10.305 3.755 L 4.799 13.381 L 3.75 13.392 Z M 10.305 5.752 L 11.981 8.708 L 11.525 9.532 L 10.319 7.408 L 7.139 13.352 L 5.951 13.367 Z M 10.347 9.459 L 10.965 10.545 L 9.423 13.323 L 8.271 13.337 Z" fill="url(%23vKxq0SU4w-1921182794-linear-gradient)" height="18px" id="vKxq0SU4w" width="20.42px"/><path d="M 0 1.002 L 0.57 0 L 16.677 0 L 18.387 1.003 L 0 1.003 Z" fill="url(%23qyqFJaVjA-1921182794-linear-gradient)" height="1.0030000000000001px" id="qyqFJaVjA" transform="translate(0 17)" width="18.387px"/><path d="M 0 1.006 L 0.567 0 L 12.545 0 L 14.254 1.006 Z" fill="url(%23KBptSRBQO-1921182794-linear-gradient)" height="1.0060000000000002px" id="KBptSRBQO" transform="translate(1 15)" width="14.254000000000005px"/><path d="M 0.578 8.79 L 4.906 1.02 L 4.325 0 L 0 7.792 Z" fill="url(%23Kgw6PgukY-1921182794-linear-gradient)" height="8.79px" id="Kgw6PgukY" transform="translate(9.5 5.5)" width="4.906000000000006px"/></g></svg>)

The Aligned Perspective

6

Read

A cohabitation agreement, created with the guidance of a financial planning advisor, provides essential protection for unmarried couples by clarifying ownership, responsibilities, and asset division.

Chief of Staff

,

Key Takeaways:

A cohabitation agreement, created with the guidance of a financial planning advisor, provides essential protection for unmarried couples by clarifying ownership, responsibilities, and asset division.

Coordinating financial planning with legal documentation—such as beneficiary designations, insurance, and estate plans—is crucial for comprehensive protection and avoiding future disputes.

Working with a fiduciary advisor experienced in unmarried couple planning ensures your agreement aligns with your values and long-term goals, offering both legal clarity and financial security.

When couples move in together, they often merge streaming accounts before discussing who owns what if they break up. How couples handle money together affects relationship outcomes, yet many lack clear agreements about property and responsibilities. A cohabitation agreement financial planning advisor helps create concrete rules about ownership and expenses that prevent future conflicts. Learn more about financial planning for major life changes at Datalign Advisory.

What a Cohabitation Agreement Advisor Does For You

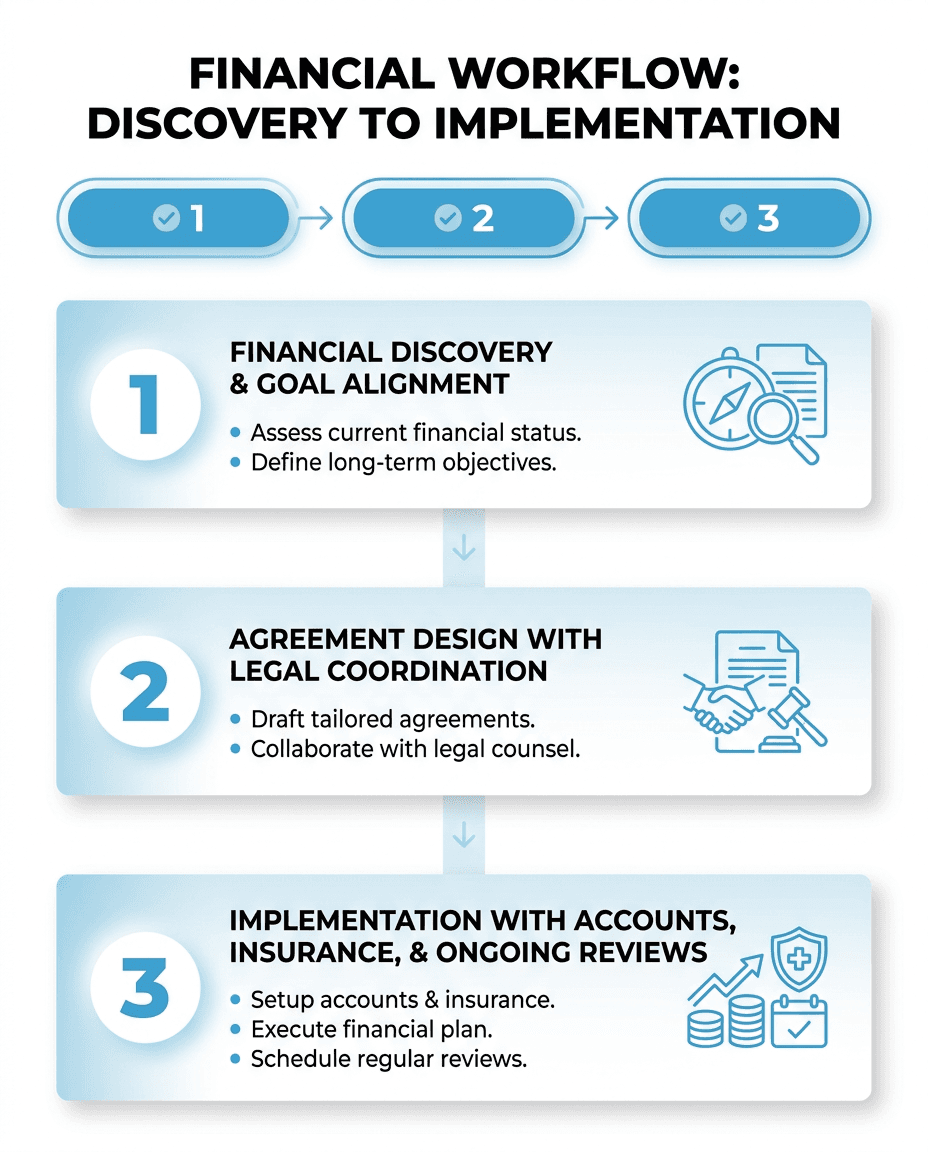

Living with your partner brings shared dreams and shared finances. But without marriage, you need someone who understands what a financial planning advisor does for a cohabitation agreement and how to protect what you're building together. An experienced advisor helps you turn your financial intentions into a solid plan that reflects your values and protects your future.

Maps Out Who Owns What and Pays What

Your advisor documents everything you own, owe, and earn to establish clear ownership rules. They help you decide which assets belong to whom and set simple rules for buying things together. Research from the Financial Planning Association shows that living together affects how couples build wealth over time. This makes the mapping process important for major life goals like buying a home or starting a business together.

Works With Lawyers to Make It Official

Your advisor teams up with an attorney to turn your financial plans into legal terms that actually work. They help design buyout formulas for shared property and establish timelines for dividing assets if you separate. The CFP Board notes that financial planners must carefully handle potential conflicts when advising couples. This includes understanding different cultural approaches to money and relationships and maintaining professional standards throughout the process.

Builds Complete Protection Plans

Beyond the agreement, your advisor aligns your insurance, emergency funds, and beneficiaries with your cohabitation terms. They make sure your investment approach matches both your shared and individual goals. According to the Journal of Accountancy, unmarried couples face unique planning challenges that require coordination between financial and legal strategies. The right advisor will also understand your background and values, helping you ask the right questions to find someone who truly gets your situation.

How Unmarried Couples Can Protect Their Finances

Working with a financial planning advisor helps you understand the gaps in legal protection that unmarried couples face. Unlike married couples, you don't have automatic rights to each other's assets, inheritance, or medical decision-making authority. How can unmarried couples protect their finances with a cohabitation agreement? The answer lies in creating explicit rules and coordinating your legal documents with your financial accounts.

Split expenses proportionally and document ownership clearly. If one partner earns significantly more, consider a percentage-based split rather than 50-50. For example, if you earn 60% of the combined income, you might pay 60% of rent and utilities. Create detailed asset inventories of who owns what, from furniture to vehicles, and attach these lists to your agreement.

Establish buyout formulas before you need them. Agree on how to value shared assets like a home or business if you separate. Many couples use the average of two independent appraisals, with specific timelines like 60 days to get estimates and 30 days to complete the buyout. This removes emotion from what can become a contentious legal process.

Coordinate your legal documents with account titling. Your cohabitation agreement provides limited protection if your bank accounts, insurance policies, and retirement plans don't reflect your intentions. Update beneficiary designations, consider joint accounts for shared expenses, and ensure your emergency fund aligns with the agreement's specified financial responsibilities.

Plan for the unexpected with insurance and estate documents. Life insurance can fund buyout provisions if one partner dies, while powers of attorney ensure you can make financial decisions for each other during emergencies. These protections become even more important when you're not legally married.

Protect Your Future With Values‑Aligned Advice

A cohabitation agreement backed by financial planning creates clear rules for your shared life and individual goals. Partnering with a fiduciary advisor who understands unmarried couples helps you build protection that matches your values.

Beyond protection, the right professional guidance transforms complex legal and wealth planning decisions into actionable steps. When you choose carefully, you get coordinated advice that protects both partners and supports long-term wealth building.

Ready to find a cohabitation agreement financial planning advisor who understands your unique situation? Datalign Advisory can connect you with a rigorously vetted, fiduciary financial advisor through our SEC-registered platform. Explore our educational resources to gain the insights you need for confident financial decisions.

Disclaimer: This information is for educational purposes only and is not intended as, nor should it be relied upon as, individualized financial, investment, tax, or legal advice, and you should consult a qualified professional about your specific circumstances before making any financial decisions.

Cohabitation Agreement And Financial Planning FAQ

Many couples have practical questions about timing, coordination, and costs when combining legal agreements with financial planning. These answers address common concerns and provide clear next steps for protecting your shared future.

Why should you consult a financial advisor before signing a cohabitation agreement?

A financial advisor maps your assets, debts, and goals before legal drafting begins. This prevents expensive legal amendments and ensures the agreement reflects realistic financial scenarios. Fiduciary advisors provide unbiased guidance on asset protection strategies that attorneys may not fully address.

How should beneficiaries, insurance coverage, and emergency funds be coordinated with the agreement?

Update beneficiary designations on retirement accounts and insurance policies to match your agreement terms. Coordinate emergency fund targets with your cost-sharing arrangements, typically 3-6 months of expenses. Estate planning coordination prevents conflicts between your agreement and existing wills or trusts.

What is the best way to handle joint purchases and gifts to avoid disputes later?

Create written agreements specifying each person's contribution percentage for major purchases over $1,000. Establish clear rules for gifts between partners versus joint gifts from others. Studies indicate unmarried couples often accumulate fewer assets than married peers, making proper documentation even more important.

When should couples start this planning process?

Begin financial discussions 3-6 months before moving in together or making major joint purchases. Life transitions require specialized advice beyond standard planning. Expect this coordination process to take 4-6 weeks and cost $500-2,000 depending on complexity.

What should you look for in a cohabitation agreement advisor?

Choose a fiduciary advisor with experience in unmarried couple planning and estate coordination. They should work collaboratively with attorneys and understand planning for couples facing unique legal and tax situations. Look for credentials like CFP certification and family law familiarity.