"/><stop offset="1" stop-color="rgb(3, 73, 122)"/></linearGradient><linearGradient id="qyqFJaVjA-1921182794-linear-gradient" x1="0" x2="1" y1="0.5558218829289385" y2="0.4441781170710614"><stop offset="0" stop-color="rgb(29, 170, 88)"/><stop offset="1" stop-color="rgb(0, 143, 203)"/></linearGradient><linearGradient id="KBptSRBQO-1921182794-linear-gradient" x1="0" x2="1" y1="0.5556785500517466" y2="0.44432144994825334"><stop offset="0" stop-color="rgb(29, 170, 88)"/><stop offset="1" stop-color="rgb(0, 143, 203)"/></linearGradient><linearGradient id="Kgw6PgukY-1921182794-linear-gradient" x1="0.2117440484028747" x2="0.7882559515971252" y1="1" y2="5.551115123125783e-17"><stop offset="0" stop-color="rgb(0, 143, 203)"/><stop offset="1" stop-color="rgb(255, 255, 255)"/></linearGradient></defs><g d="M 25.388 5.232 L 25.388 10.89 L 26.819 10.89 C 29.017 10.89 30.33 9.837 30.33 8.061 C 30.33 6.285 28.996 5.232 26.766 5.232 L 25.387 5.232 Z M 24 12.008 L 24 4.118 L 26.79 4.118 C 29.895 4.118 31.746 5.599 31.746 8.065 C 31.746 10.53 29.916 12.012 26.844 12.012 L 24 12.012 Z M 38.74 9.415 C 38.233 8.438 37.652 7.265 37.166 6.248 C 36.665 7.317 36.137 8.373 35.582 9.415 Z M 37.113 4 L 37.22 4 L 41.53 12.015 L 40.064 12.015 L 39.179 10.413 L 35.129 10.413 L 34.266 12.015 L 32.799 12.015 L 37.109 4 Z M 45.954 5.232 L 45.954 12.008 L 44.567 12.008 L 44.567 5.232 L 41.809 5.232 L 41.809 4.118 L 48.714 4.118 L 48.714 5.232 L 45.955 5.232 Z M 54.927 9.415 C 54.421 8.438 53.84 7.265 53.354 6.248 C 52.853 7.317 52.324 8.373 51.77 9.415 L 54.928 9.415 Z M 53.302 4 L 53.409 4 L 57.719 12.015 L 56.256 12.015 L 55.371 10.413 L 51.321 10.413 L 50.458 12.015 L 48.992 12.015 Z M 59.88 12.008 L 59.88 4.114 L 61.268 4.114 L 61.268 10.89 L 65.158 10.89 L 65.158 12.008 Z M 68.892 4.5 L 67.5 4.5 L 67.5 12.39 L 68.892 12.39 Z M 76.924 12.177 C 73.994 12.177 72 10.522 72 8.089 C 72 5.656 74.002 4 76.935 4 C 78.326 4 79.208 4.305 79.779 4.57 L 79.779 5.808 C 78.894 5.415 77.935 5.214 76.967 5.217 C 74.844 5.217 73.403 6.379 73.403 8.089 C 73.403 9.799 74.826 10.972 76.924 10.972 C 77.495 10.972 78.216 10.874 78.658 10.732 L 78.658 8.408 L 79.993 8.408 L 79.993 11.578 C 79.218 11.942 77.97 12.181 76.924 12.181 M 85.16 7.698 C 84.792 7.368 84.385 7.03 84.157 6.808 C 84.157 7.106 84.167 7.586 84.167 7.905 L 84.167 12.038 L 82.791 12.038 L 82.791 4.024 L 82.888 4.024 L 87.844 8.475 L 88.836 9.376 C 88.825 9.071 88.825 8.664 88.825 8.279 L 88.825 4.147 L 90.201 4.147 L 90.201 12.161 L 90.116 12.161 L 85.159 7.698 Z M 42 17.859 L 43.799 14.508 L 43.941 14.508 L 45.743 17.859 L 44.98 17.859 L 44.627 17.224 L 43.107 17.224 L 42.764 17.859 Z M 44.366 16.661 C 44.198 16.331 44.034 16 43.874 15.666 C 43.72 15.993 43.542 16.346 43.378 16.661 Z M 47.799 14.555 C 49.09 14.555 49.85 15.18 49.85 16.207 C 49.85 17.235 49.097 17.859 47.82 17.859 L 46.607 17.859 L 46.607 14.555 Z M 47.32 15.161 L 47.32 17.249 L 47.81 17.249 C 48.63 17.249 49.13 16.868 49.13 16.204 C 49.13 15.539 48.623 15.158 47.791 15.158 L 47.321 15.158 L 47.321 15.161 Z M 52.07 17.907 L 52.087 17.874 L 50.307 14.554 L 51.085 14.554 L 51.795 15.913 C 51.941 16.2 52.059 16.425 52.177 16.672 C 52.341 16.327 52.527 15.986 52.751 15.553 L 53.271 14.558 L 54.05 14.558 L 52.251 17.91 L 52.07 17.91 Z M 55.584 17.859 L 54.87 17.859 L 54.87 14.555 L 55.584 14.555 Z M 56.804 17.739 L 56.726 17.71 L 56.726 17.02 L 56.836 17.068 C 57.146 17.198 57.536 17.286 57.86 17.286 C 58.082 17.286 58.26 17.253 58.381 17.195 C 58.478 17.144 58.535 17.079 58.535 16.988 C 58.535 16.886 58.495 16.81 58.395 16.741 C 58.278 16.657 58.085 16.585 57.793 16.498 C 57.029 16.276 56.697 15.996 56.697 15.459 C 56.697 14.875 57.193 14.5 58.028 14.5 C 58.363 14.5 58.724 14.562 58.984 14.668 L 59.034 14.686 L 59.034 15.357 L 58.924 15.307 C 58.648 15.188 58.35 15.126 58.049 15.125 C 57.839 15.125 57.668 15.155 57.55 15.219 C 57.454 15.27 57.396 15.343 57.396 15.437 C 57.396 15.528 57.436 15.601 57.532 15.673 C 57.65 15.761 57.839 15.84 58.128 15.928 C 58.884 16.156 59.234 16.425 59.234 16.951 C 59.234 17.551 58.742 17.914 57.882 17.914 C 57.514 17.914 57.104 17.844 56.801 17.736 Z M 62.089 14.5 C 63.273 14.5 64.076 15.198 64.076 16.21 C 64.076 17.224 63.27 17.921 62.089 17.921 C 60.908 17.921 60.101 17.224 60.101 16.211 C 60.101 15.198 60.907 14.501 62.088 14.501 Z M 62.089 17.271 C 62.834 17.271 63.352 16.846 63.352 16.211 C 63.352 15.575 62.834 15.147 62.088 15.147 C 61.343 15.147 60.818 15.572 60.818 16.211 C 60.818 16.85 61.339 17.271 62.088 17.271 Z M 66.499 14.558 C 67.373 14.558 67.908 14.954 67.908 15.63 C 67.908 16.073 67.64 16.41 67.188 16.567 L 68.043 17.863 L 67.255 17.863 L 66.505 16.683 L 65.906 16.683 L 65.906 17.863 L 65.2 17.863 L 65.2 14.559 L 66.499 14.559 Z M 65.906 15.165 L 65.906 16.098 L 66.527 16.098 C 66.93 16.098 67.194 15.938 67.194 15.63 C 67.194 15.321 66.924 15.165 66.502 15.165 Z M 69.325 14.591 L 70.263 15.935 L 71.23 14.558 L 72.047 14.558 L 70.62 16.574 L 70.62 17.863 L 69.906 17.863 L 69.906 16.573 L 68.479 14.559 L 69.296 14.559 L 69.321 14.591 Z M 2.034 14.412 L 9.998 14.325 L 11.532 11.558 L 13.58 15.168 L 1.602 15.168 L 1.032 16.17 L 15.285 16.17 L 12.092 10.541 L 12.549 9.717 L 16.673 16.987 L 0.571 16.987 L 0 17.989 L 18.386 17.989 L 13.116 8.7 L 13.559 7.902 L 19.285 18 L 20.42 18 L 10.212 0 Z M 10.212 2.004 L 12.984 6.896 L 12.542 7.695 L 10.305 3.755 L 4.799 13.381 L 3.75 13.392 Z M 10.305 5.752 L 11.981 8.708 L 11.525 9.532 L 10.319 7.408 L 7.139 13.352 L 5.951 13.367 Z M 10.347 9.459 L 10.965 10.545 L 9.423 13.323 L 8.271 13.337 Z M 0 18.002 L 0.57 17 L 16.677 17 L 18.387 18.003 L 0 18.003 Z M 1 16.006 L 1.567 15 L 13.545 15 L 15.254 16.006 Z M 10.078 14.29 L 14.406 6.52 L 13.825 5.5 L 9.5 13.292 Z" fill="transparent" height="18.003px" id="K_8etyHP8" width="90.20100036621093px"><path d="M 1.388 1.232 L 1.388 6.89 L 2.819 6.89 C 5.017 6.89 6.33 5.837 6.33 4.061 C 6.33 2.285 4.996 1.232 2.766 1.232 L 1.387 1.232 Z M 0 8.008 L 0 0.118 L 2.79 0.118 C 5.895 0.118 7.746 1.599 7.746 4.065 C 7.746 6.53 5.916 8.012 2.844 8.012 L 0 8.012 Z M 14.74 5.415 C 14.233 4.438 13.652 3.265 13.166 2.248 C 12.665 3.317 12.137 4.373 11.582 5.415 Z M 13.113 0 L 13.22 0 L 17.53 8.015 L 16.064 8.015 L 15.179 6.413 L 11.129 6.413 L 10.266 8.015 L 8.799 8.015 L 13.109 0 Z M 21.954 1.232 L 21.954 8.008 L 20.567 8.008 L 20.567 1.232 L 17.809 1.232 L 17.809 0.118 L 24.714 0.118 L 24.714 1.232 L 21.955 1.232 Z M 30.927 5.415 C 30.421 4.438 29.84 3.265 29.354 2.248 C 28.853 3.317 28.324 4.373 27.77 5.415 L 30.928 5.415 Z M 29.302 0 L 29.409 0 L 33.719 8.015 L 32.256 8.015 L 31.371 6.413 L 27.321 6.413 L 26.458 8.015 L 24.992 8.015 Z M 35.88 8.008 L 35.88 0.114 L 37.268 0.114 L 37.268 6.89 L 41.158 6.89 L 41.158 8.008 Z" fill="rgb(132, 130, 142)" height="8.015px" id="jAL5eYCXu" transform="translate(24 4)" width="41.15800106811523px"/><path d="M 1.392 0 L 0 0 L 0 7.89 L 1.392 7.89 Z" fill="rgb(132, 130, 142)" height="7.890000000000001px" id="u8cKeOXNI" transform="translate(67.5 4.5)" width="1.391999999999996px"/><path d="M 4.924 8.177 C 1.994 8.177 0 6.522 0 4.089 C 0 1.656 2.002 0 4.935 0 C 6.326 0 7.208 0.305 7.779 0.57 L 7.779 1.808 C 6.894 1.415 5.935 1.214 4.967 1.217 C 2.844 1.217 1.403 2.379 1.403 4.089 C 1.403 5.799 2.826 6.972 4.924 6.972 C 5.495 6.972 6.216 6.874 6.658 6.732 L 6.658 4.408 L 7.993 4.408 L 7.993 7.578 C 7.218 7.942 5.97 8.181 4.924 8.181 M 13.16 3.698 C 12.792 3.368 12.385 3.03 12.157 2.808 C 12.157 3.106 12.167 3.586 12.167 3.905 L 12.167 8.038 L 10.791 8.038 L 10.791 0.024 L 10.888 0.024 L 15.844 4.475 L 16.836 5.376 C 16.825 5.071 16.825 4.664 16.825 4.279 L 16.825 0.147 L 18.201 0.147 L 18.201 8.161 L 18.116 8.161 L 13.159 3.698 Z" fill="rgb(132, 130, 142)" height="8.181px" id="kN7yl8Gfy" transform="translate(72 4)" width="18.201000366210934px"/><path d="M 0 3.359 L 1.799 0.008 L 1.941 0.008 L 3.743 3.359 L 2.98 3.359 L 2.627 2.724 L 1.107 2.724 L 0.764 3.359 Z M 2.366 2.161 C 2.198 1.831 2.034 1.5 1.874 1.166 C 1.72 1.493 1.542 1.846 1.378 2.161 Z M 5.799 0.055 C 7.09 0.055 7.85 0.68 7.85 1.707 C 7.85 2.735 7.097 3.359 5.82 3.359 L 4.607 3.359 L 4.607 0.055 Z M 5.32 0.661 L 5.32 2.749 L 5.81 2.749 C 6.63 2.749 7.13 2.368 7.13 1.704 C 7.13 1.039 6.623 0.658 5.791 0.658 L 5.321 0.658 L 5.321 0.661 Z M 10.07 3.407 L 10.087 3.374 L 8.307 0.054 L 9.085 0.054 L 9.795 1.413 C 9.941 1.7 10.059 1.925 10.177 2.172 C 10.341 1.827 10.527 1.486 10.751 1.053 L 11.271 0.058 L 12.05 0.058 L 10.251 3.41 L 10.07 3.41 Z M 13.584 3.359 L 12.87 3.359 L 12.87 0.055 L 13.584 0.055 Z M 14.804 3.239 L 14.726 3.21 L 14.726 2.52 L 14.836 2.568 C 15.146 2.698 15.536 2.786 15.86 2.786 C 16.082 2.786 16.26 2.753 16.381 2.695 C 16.478 2.644 16.535 2.579 16.535 2.488 C 16.535 2.386 16.495 2.31 16.395 2.241 C 16.278 2.157 16.085 2.085 15.793 1.998 C 15.029 1.776 14.697 1.496 14.697 0.959 C 14.697 0.375 15.193 0 16.028 0 C 16.363 0 16.724 0.062 16.984 0.168 L 17.034 0.186 L 17.034 0.857 L 16.924 0.807 C 16.648 0.688 16.35 0.626 16.049 0.625 C 15.839 0.625 15.668 0.655 15.55 0.719 C 15.454 0.77 15.396 0.843 15.396 0.937 C 15.396 1.028 15.436 1.101 15.532 1.173 C 15.65 1.261 15.839 1.34 16.128 1.428 C 16.884 1.656 17.234 1.925 17.234 2.451 C 17.234 3.051 16.742 3.414 15.882 3.414 C 15.514 3.414 15.104 3.344 14.801 3.236 Z M 20.089 0 C 21.273 0 22.076 0.698 22.076 1.71 C 22.076 2.724 21.27 3.421 20.089 3.421 C 18.908 3.421 18.101 2.724 18.101 1.711 C 18.101 0.698 18.907 0.001 20.088 0.001 Z M 20.089 2.771 C 20.834 2.771 21.352 2.346 21.352 1.711 C 21.352 1.075 20.834 0.647 20.088 0.647 C 19.343 0.647 18.818 1.072 18.818 1.711 C 18.818 2.35 19.339 2.771 20.088 2.771 Z M 24.499 0.058 C 25.373 0.058 25.908 0.454 25.908 1.13 C 25.908 1.573 25.64 1.91 25.188 2.067 L 26.043 3.363 L 25.255 3.363 L 24.505 2.183 L 23.906 2.183 L 23.906 3.363 L 23.2 3.363 L 23.2 0.059 L 24.499 0.059 Z M 23.906 0.665 L 23.906 1.598 L 24.527 1.598 C 24.93 1.598 25.194 1.438 25.194 1.13 C 25.194 0.821 24.924 0.665 24.502 0.665 Z M 27.325 0.091 L 28.263 1.435 L 29.23 0.058 L 30.047 0.058 L 28.62 2.074 L 28.62 3.363 L 27.906 3.363 L 27.906 2.073 L 26.479 0.059 L 27.296 0.059 L 27.321 0.091 Z" fill="rgb(142, 140, 153)" height="3.421000000000001px" id="P22Fbj16y" transform="translate(42 14.5)" width="30.047000091552746px"/><path d="M 2.034 14.412 L 9.998 14.325 L 11.532 11.558 L 13.58 15.168 L 1.602 15.168 L 1.032 16.17 L 15.285 16.17 L 12.092 10.541 L 12.549 9.717 L 16.673 16.987 L 0.571 16.987 L 0 17.989 L 18.386 17.989 L 13.116 8.7 L 13.559 7.902 L 19.285 18 L 20.42 18 L 10.212 0 Z M 10.212 2.004 L 12.984 6.896 L 12.542 7.695 L 10.305 3.755 L 4.799 13.381 L 3.75 13.392 Z M 10.305 5.752 L 11.981 8.708 L 11.525 9.532 L 10.319 7.408 L 7.139 13.352 L 5.951 13.367 Z M 10.347 9.459 L 10.965 10.545 L 9.423 13.323 L 8.271 13.337 Z" fill="url(%23vKxq0SU4w-1921182794-linear-gradient)" height="18px" id="vKxq0SU4w" width="20.42px"/><path d="M 0 1.002 L 0.57 0 L 16.677 0 L 18.387 1.003 L 0 1.003 Z" fill="url(%23qyqFJaVjA-1921182794-linear-gradient)" height="1.0030000000000001px" id="qyqFJaVjA" transform="translate(0 17)" width="18.387px"/><path d="M 0 1.006 L 0.567 0 L 12.545 0 L 14.254 1.006 Z" fill="url(%23KBptSRBQO-1921182794-linear-gradient)" height="1.0060000000000002px" id="KBptSRBQO" transform="translate(1 15)" width="14.254000000000005px"/><path d="M 0.578 8.79 L 4.906 1.02 L 4.325 0 L 0 7.792 Z" fill="url(%23Kgw6PgukY-1921182794-linear-gradient)" height="8.79px" id="Kgw6PgukY" transform="translate(9.5 5.5)" width="4.906000000000006px"/></g></svg>)

The Aligned Perspective

Fiduciary financial advisors are legally obligated to put your interests first, providing advice free from conflicts of interest.

Director of Customer Success

,

Key Takeaways:

Fiduciary financial advisors are legally obligated to put your interests first, providing advice free from conflicts of interest and prioritizing your financial well-being.

Understanding the differences between fiduciary and non-fiduciary advisors—especially in compensation and disclosure—helps you make informed decisions and avoid hidden conflicts.

You can verify an advisor's fiduciary status in minutes by checking SEC databases, reviewing disclosures, and requesting written confirmation of their commitment to act in your best interest.

When building wealth while supporting family, you need advice that actually serves your interests, not hidden sales goals. The solution lies in understanding fiduciary duty, which legally requires advisors to put your needs first. This approach aligns advice with your values while reducing conflicts that could derail your progress.

Explore educational resources at Datalign Advisory to prepare for your advisor search.

What Does a Fiduciary Financial Advisor Do? Duties, Standards, and Real-World Impact

Understanding what a fiduciary financial advisor does goes beyond legal definitions. These advisors operate under specific duties that shape every recommendation, from investment selection to fee disclosure, creating a foundation of trust that supports your wealth-building journey.

Core Fiduciary Duties Guide Every Decision

Fiduciary advisors must follow three core duties: loyalty (putting your interests first), prudence (using professional care), and full disclosure of conflicts. They cannot recommend investments that benefit them more than you.

These Duties Are Enforced Differently Across Advisor Types

Investment advisers must always act as fiduciaries, while brokers follow different standards that only apply to specific transactions. Understanding these differences helps you choose the right type of advisor for your needs and know what level of protection to expect.

Real-World Impact for Wealth Building

A fiduciary can coordinate your 401(k), Roth IRA, and family support goals while honoring your values around sustainability. For instance, when choosing between investment options for your Roth IRA, a fiduciary must recommend based on your goals, not which option pays them higher fees. They must also explain how their compensation might influence their advice.

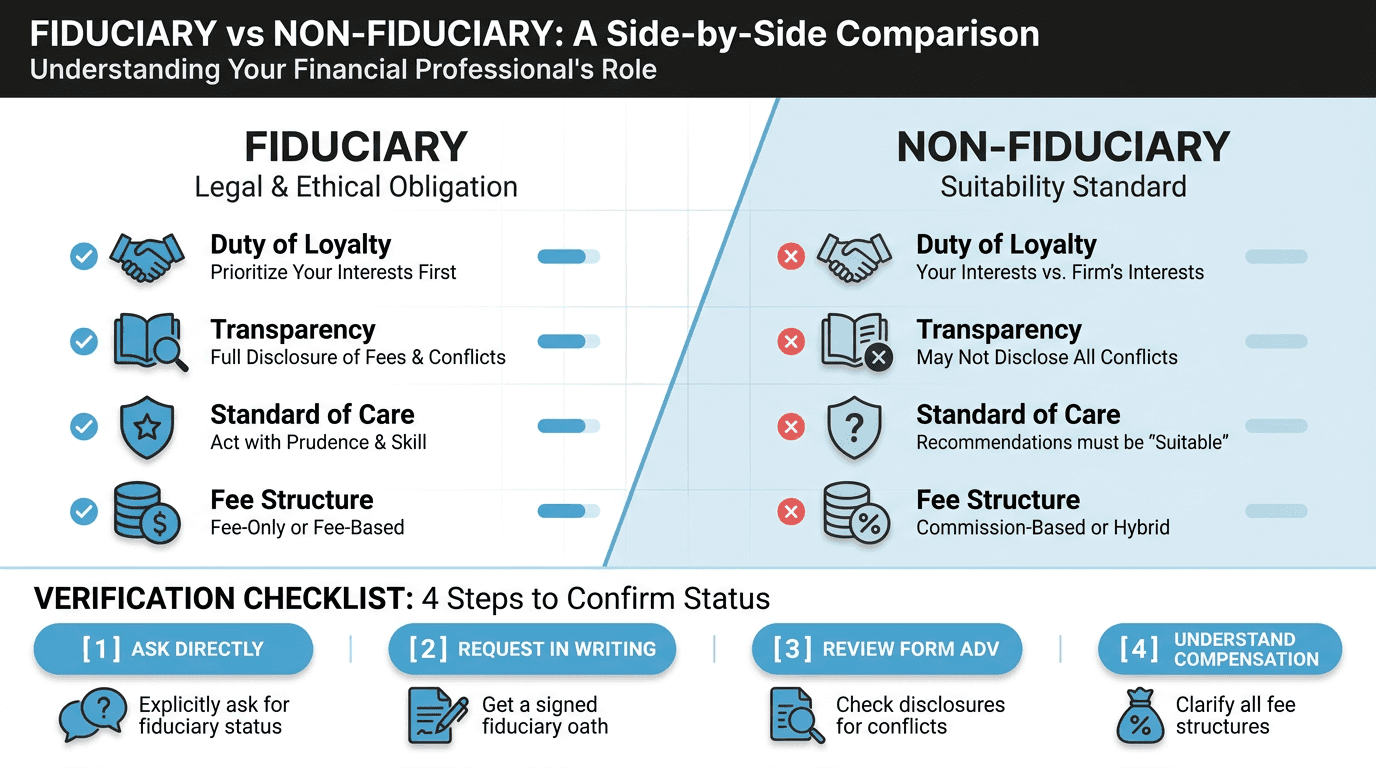

Fiduciary vs Non-Fiduciary: Key Differences and How To Verify in 10 Minutes

Understanding how a fiduciary financial advisor is different from a non-fiduciary comes down to legal obligations and compensation structures. While both can provide valuable advice, fiduciaries operate under stricter standards that reduce conflicts and require transparent fee disclosure. Here's what to look for and how to verify an advisor's status quickly.

Key Differences That Impact Your Money:

Conflict management: Fiduciaries must disclose all conflicts and prioritize your interests, while non-fiduciaries can recommend products that pay them higher commissions without the same disclosure requirements.

Fee transparency: Fee-only fiduciaries charge clear advisory fees with no hidden commissions, while commission-based advisors earn money from product sales that may not align with your goals.

Ongoing obligation: Fiduciary duty applies to the entire advisory relationship, not just individual transactions, creating consistent protection for your financial decisions.

Legal standard: Fiduciaries face stricter regulatory oversight and potential liability, while non-fiduciaries may only need to meet suitability standards for specific recommendations.

Once you understand these differences, you can verify an advisor's fiduciary status using this practical checklist:

Search SEC records: Use the SEC's IAPD database to confirm registration and review any disciplinary history or client complaints.

Request Form ADV Part 2A: This document reveals fee structures, conflicts of interest, and services offered, giving you a complete picture of how the advisor operates.

Ask for written fiduciary acknowledgment: Request a signed statement confirming they will act as a fiduciary for all services, not just investment management.

Confirm coverage scope: Verify that fiduciary duty applies to financial planning, not just investment advice, especially if you need help coordinating multiple financial goals.

Find a Fiduciary Financial Advisor Aligned With Your Goals

A fiduciary financial advisor puts your interests first through legal duties of loyalty and care, reducing conflicts compared to non-fiduciary models. Verification through SEC databases and written confirmation helps ensure you're working with a true fiduciary.

When you're ready to find a fiduciary financial advisor, verify their registration through the SEC's investor database and request written confirmation of their fiduciary duty. Datalign Advisory can connect you with a rigorously vetted fiduciary advisor who aligns with your goals, preferences, and values through our SEC-registered platform.

Ready to take the next step? Explore Educational Resources from Datalign Advisory to prepare for your first conversation with a trusted fiduciary advisor.

Fiduciary Financial Advisor FAQs

When you're building wealth and supporting family goals, understanding fiduciary standards can protect your financial progress. These answers address the most common questions that emerging wealth builders ask about advisor obligations, costs, and verification.

How is fiduciary duty different from Regulation Best Interest?

Fiduciary advisors must put your interests first in every recommendation and ongoing advice, while Regulation Best Interest applies to broker-dealers for specific recommendations only. Fiduciary advisors must avoid conflicts or fully disclose them, whereas Reg BI allows certain conflicts if disclosed. This matters for your long-term plan because fiduciary coverage extends to ongoing advice and planning, not just individual transactions.

What's the difference between fee-only, fee-based, and commission models?

Fee-only advisors receive compensation directly from you, which usually aligns with fiduciary duty since they don't earn commissions from product sales. Fee-based advisors can charge fees and receive commissions, creating potential conflicts. Commission-only advisors earn money from product sales, which may not prioritize your interests. Ask about all compensation sources and request written confirmation of advisor compensation models regardless of fee structure.

How can I verify an advisor's fiduciary commitment?

Check the SEC's IAPD database to confirm registration and review Form ADV Part 2A for fee disclosures and conflicts. Request a written acknowledgment that the advisor will act as a fiduciary for all services, not just investment management. Ask specifically: "Will you provide a written commitment to act in my best interest at all times?" Platforms like Datalign can connect you with pre-vetted fiduciary advisors, and fee-only advisors often provide clearer fiduciary alignment.

What questions should I ask about total costs?

Request a breakdown of all fees, including management fees, planning fees, and any third-party costs. Ask: "What will I pay annually in total dollars and as a percentage of my assets?" Also inquire about fee increases and billing frequency. Understanding total compensation helps you compare advisors and ensures cost transparency.

Why does fiduciary duty matter for long-term financial planning?

Fiduciary duty creates legal accountability for advice that serves your interests, not the advisor's compensation. This protection becomes more valuable as your wealth grows and decisions become more complex. A fiduciary must consider your entire financial picture, including family support goals and values-based investing, rather than focusing on products that generate higher commissions.

Disclaimer: This information is for educational purposes only and is not intended as, nor should it be relied upon as, individualized financial, investment, tax, or legal advice, and you should consult a qualified professional about your specific circumstances before making any financial decisions.