"/><stop offset="1" stop-color="rgb(3, 73, 122)"/></linearGradient><linearGradient id="qyqFJaVjA-1921182794-linear-gradient" x1="0" x2="1" y1="0.5558218829289385" y2="0.4441781170710614"><stop offset="0" stop-color="rgb(29, 170, 88)"/><stop offset="1" stop-color="rgb(0, 143, 203)"/></linearGradient><linearGradient id="KBptSRBQO-1921182794-linear-gradient" x1="0" x2="1" y1="0.5556785500517466" y2="0.44432144994825334"><stop offset="0" stop-color="rgb(29, 170, 88)"/><stop offset="1" stop-color="rgb(0, 143, 203)"/></linearGradient><linearGradient id="Kgw6PgukY-1921182794-linear-gradient" x1="0.2117440484028747" x2="0.7882559515971252" y1="1" y2="5.551115123125783e-17"><stop offset="0" stop-color="rgb(0, 143, 203)"/><stop offset="1" stop-color="rgb(255, 255, 255)"/></linearGradient></defs><g d="M 25.388 5.232 L 25.388 10.89 L 26.819 10.89 C 29.017 10.89 30.33 9.837 30.33 8.061 C 30.33 6.285 28.996 5.232 26.766 5.232 L 25.387 5.232 Z M 24 12.008 L 24 4.118 L 26.79 4.118 C 29.895 4.118 31.746 5.599 31.746 8.065 C 31.746 10.53 29.916 12.012 26.844 12.012 L 24 12.012 Z M 38.74 9.415 C 38.233 8.438 37.652 7.265 37.166 6.248 C 36.665 7.317 36.137 8.373 35.582 9.415 Z M 37.113 4 L 37.22 4 L 41.53 12.015 L 40.064 12.015 L 39.179 10.413 L 35.129 10.413 L 34.266 12.015 L 32.799 12.015 L 37.109 4 Z M 45.954 5.232 L 45.954 12.008 L 44.567 12.008 L 44.567 5.232 L 41.809 5.232 L 41.809 4.118 L 48.714 4.118 L 48.714 5.232 L 45.955 5.232 Z M 54.927 9.415 C 54.421 8.438 53.84 7.265 53.354 6.248 C 52.853 7.317 52.324 8.373 51.77 9.415 L 54.928 9.415 Z M 53.302 4 L 53.409 4 L 57.719 12.015 L 56.256 12.015 L 55.371 10.413 L 51.321 10.413 L 50.458 12.015 L 48.992 12.015 Z M 59.88 12.008 L 59.88 4.114 L 61.268 4.114 L 61.268 10.89 L 65.158 10.89 L 65.158 12.008 Z M 68.892 4.5 L 67.5 4.5 L 67.5 12.39 L 68.892 12.39 Z M 76.924 12.177 C 73.994 12.177 72 10.522 72 8.089 C 72 5.656 74.002 4 76.935 4 C 78.326 4 79.208 4.305 79.779 4.57 L 79.779 5.808 C 78.894 5.415 77.935 5.214 76.967 5.217 C 74.844 5.217 73.403 6.379 73.403 8.089 C 73.403 9.799 74.826 10.972 76.924 10.972 C 77.495 10.972 78.216 10.874 78.658 10.732 L 78.658 8.408 L 79.993 8.408 L 79.993 11.578 C 79.218 11.942 77.97 12.181 76.924 12.181 M 85.16 7.698 C 84.792 7.368 84.385 7.03 84.157 6.808 C 84.157 7.106 84.167 7.586 84.167 7.905 L 84.167 12.038 L 82.791 12.038 L 82.791 4.024 L 82.888 4.024 L 87.844 8.475 L 88.836 9.376 C 88.825 9.071 88.825 8.664 88.825 8.279 L 88.825 4.147 L 90.201 4.147 L 90.201 12.161 L 90.116 12.161 L 85.159 7.698 Z M 42 17.859 L 43.799 14.508 L 43.941 14.508 L 45.743 17.859 L 44.98 17.859 L 44.627 17.224 L 43.107 17.224 L 42.764 17.859 Z M 44.366 16.661 C 44.198 16.331 44.034 16 43.874 15.666 C 43.72 15.993 43.542 16.346 43.378 16.661 Z M 47.799 14.555 C 49.09 14.555 49.85 15.18 49.85 16.207 C 49.85 17.235 49.097 17.859 47.82 17.859 L 46.607 17.859 L 46.607 14.555 Z M 47.32 15.161 L 47.32 17.249 L 47.81 17.249 C 48.63 17.249 49.13 16.868 49.13 16.204 C 49.13 15.539 48.623 15.158 47.791 15.158 L 47.321 15.158 L 47.321 15.161 Z M 52.07 17.907 L 52.087 17.874 L 50.307 14.554 L 51.085 14.554 L 51.795 15.913 C 51.941 16.2 52.059 16.425 52.177 16.672 C 52.341 16.327 52.527 15.986 52.751 15.553 L 53.271 14.558 L 54.05 14.558 L 52.251 17.91 L 52.07 17.91 Z M 55.584 17.859 L 54.87 17.859 L 54.87 14.555 L 55.584 14.555 Z M 56.804 17.739 L 56.726 17.71 L 56.726 17.02 L 56.836 17.068 C 57.146 17.198 57.536 17.286 57.86 17.286 C 58.082 17.286 58.26 17.253 58.381 17.195 C 58.478 17.144 58.535 17.079 58.535 16.988 C 58.535 16.886 58.495 16.81 58.395 16.741 C 58.278 16.657 58.085 16.585 57.793 16.498 C 57.029 16.276 56.697 15.996 56.697 15.459 C 56.697 14.875 57.193 14.5 58.028 14.5 C 58.363 14.5 58.724 14.562 58.984 14.668 L 59.034 14.686 L 59.034 15.357 L 58.924 15.307 C 58.648 15.188 58.35 15.126 58.049 15.125 C 57.839 15.125 57.668 15.155 57.55 15.219 C 57.454 15.27 57.396 15.343 57.396 15.437 C 57.396 15.528 57.436 15.601 57.532 15.673 C 57.65 15.761 57.839 15.84 58.128 15.928 C 58.884 16.156 59.234 16.425 59.234 16.951 C 59.234 17.551 58.742 17.914 57.882 17.914 C 57.514 17.914 57.104 17.844 56.801 17.736 Z M 62.089 14.5 C 63.273 14.5 64.076 15.198 64.076 16.21 C 64.076 17.224 63.27 17.921 62.089 17.921 C 60.908 17.921 60.101 17.224 60.101 16.211 C 60.101 15.198 60.907 14.501 62.088 14.501 Z M 62.089 17.271 C 62.834 17.271 63.352 16.846 63.352 16.211 C 63.352 15.575 62.834 15.147 62.088 15.147 C 61.343 15.147 60.818 15.572 60.818 16.211 C 60.818 16.85 61.339 17.271 62.088 17.271 Z M 66.499 14.558 C 67.373 14.558 67.908 14.954 67.908 15.63 C 67.908 16.073 67.64 16.41 67.188 16.567 L 68.043 17.863 L 67.255 17.863 L 66.505 16.683 L 65.906 16.683 L 65.906 17.863 L 65.2 17.863 L 65.2 14.559 L 66.499 14.559 Z M 65.906 15.165 L 65.906 16.098 L 66.527 16.098 C 66.93 16.098 67.194 15.938 67.194 15.63 C 67.194 15.321 66.924 15.165 66.502 15.165 Z M 69.325 14.591 L 70.263 15.935 L 71.23 14.558 L 72.047 14.558 L 70.62 16.574 L 70.62 17.863 L 69.906 17.863 L 69.906 16.573 L 68.479 14.559 L 69.296 14.559 L 69.321 14.591 Z M 2.034 14.412 L 9.998 14.325 L 11.532 11.558 L 13.58 15.168 L 1.602 15.168 L 1.032 16.17 L 15.285 16.17 L 12.092 10.541 L 12.549 9.717 L 16.673 16.987 L 0.571 16.987 L 0 17.989 L 18.386 17.989 L 13.116 8.7 L 13.559 7.902 L 19.285 18 L 20.42 18 L 10.212 0 Z M 10.212 2.004 L 12.984 6.896 L 12.542 7.695 L 10.305 3.755 L 4.799 13.381 L 3.75 13.392 Z M 10.305 5.752 L 11.981 8.708 L 11.525 9.532 L 10.319 7.408 L 7.139 13.352 L 5.951 13.367 Z M 10.347 9.459 L 10.965 10.545 L 9.423 13.323 L 8.271 13.337 Z M 0 18.002 L 0.57 17 L 16.677 17 L 18.387 18.003 L 0 18.003 Z M 1 16.006 L 1.567 15 L 13.545 15 L 15.254 16.006 Z M 10.078 14.29 L 14.406 6.52 L 13.825 5.5 L 9.5 13.292 Z" fill="transparent" height="18.003px" id="K_8etyHP8" width="90.20100036621093px"><path d="M 1.388 1.232 L 1.388 6.89 L 2.819 6.89 C 5.017 6.89 6.33 5.837 6.33 4.061 C 6.33 2.285 4.996 1.232 2.766 1.232 L 1.387 1.232 Z M 0 8.008 L 0 0.118 L 2.79 0.118 C 5.895 0.118 7.746 1.599 7.746 4.065 C 7.746 6.53 5.916 8.012 2.844 8.012 L 0 8.012 Z M 14.74 5.415 C 14.233 4.438 13.652 3.265 13.166 2.248 C 12.665 3.317 12.137 4.373 11.582 5.415 Z M 13.113 0 L 13.22 0 L 17.53 8.015 L 16.064 8.015 L 15.179 6.413 L 11.129 6.413 L 10.266 8.015 L 8.799 8.015 L 13.109 0 Z M 21.954 1.232 L 21.954 8.008 L 20.567 8.008 L 20.567 1.232 L 17.809 1.232 L 17.809 0.118 L 24.714 0.118 L 24.714 1.232 L 21.955 1.232 Z M 30.927 5.415 C 30.421 4.438 29.84 3.265 29.354 2.248 C 28.853 3.317 28.324 4.373 27.77 5.415 L 30.928 5.415 Z M 29.302 0 L 29.409 0 L 33.719 8.015 L 32.256 8.015 L 31.371 6.413 L 27.321 6.413 L 26.458 8.015 L 24.992 8.015 Z M 35.88 8.008 L 35.88 0.114 L 37.268 0.114 L 37.268 6.89 L 41.158 6.89 L 41.158 8.008 Z" fill="rgb(132, 130, 142)" height="8.015px" id="jAL5eYCXu" transform="translate(24 4)" width="41.15800106811523px"/><path d="M 1.392 0 L 0 0 L 0 7.89 L 1.392 7.89 Z" fill="rgb(132, 130, 142)" height="7.890000000000001px" id="u8cKeOXNI" transform="translate(67.5 4.5)" width="1.391999999999996px"/><path d="M 4.924 8.177 C 1.994 8.177 0 6.522 0 4.089 C 0 1.656 2.002 0 4.935 0 C 6.326 0 7.208 0.305 7.779 0.57 L 7.779 1.808 C 6.894 1.415 5.935 1.214 4.967 1.217 C 2.844 1.217 1.403 2.379 1.403 4.089 C 1.403 5.799 2.826 6.972 4.924 6.972 C 5.495 6.972 6.216 6.874 6.658 6.732 L 6.658 4.408 L 7.993 4.408 L 7.993 7.578 C 7.218 7.942 5.97 8.181 4.924 8.181 M 13.16 3.698 C 12.792 3.368 12.385 3.03 12.157 2.808 C 12.157 3.106 12.167 3.586 12.167 3.905 L 12.167 8.038 L 10.791 8.038 L 10.791 0.024 L 10.888 0.024 L 15.844 4.475 L 16.836 5.376 C 16.825 5.071 16.825 4.664 16.825 4.279 L 16.825 0.147 L 18.201 0.147 L 18.201 8.161 L 18.116 8.161 L 13.159 3.698 Z" fill="rgb(132, 130, 142)" height="8.181px" id="kN7yl8Gfy" transform="translate(72 4)" width="18.201000366210934px"/><path d="M 0 3.359 L 1.799 0.008 L 1.941 0.008 L 3.743 3.359 L 2.98 3.359 L 2.627 2.724 L 1.107 2.724 L 0.764 3.359 Z M 2.366 2.161 C 2.198 1.831 2.034 1.5 1.874 1.166 C 1.72 1.493 1.542 1.846 1.378 2.161 Z M 5.799 0.055 C 7.09 0.055 7.85 0.68 7.85 1.707 C 7.85 2.735 7.097 3.359 5.82 3.359 L 4.607 3.359 L 4.607 0.055 Z M 5.32 0.661 L 5.32 2.749 L 5.81 2.749 C 6.63 2.749 7.13 2.368 7.13 1.704 C 7.13 1.039 6.623 0.658 5.791 0.658 L 5.321 0.658 L 5.321 0.661 Z M 10.07 3.407 L 10.087 3.374 L 8.307 0.054 L 9.085 0.054 L 9.795 1.413 C 9.941 1.7 10.059 1.925 10.177 2.172 C 10.341 1.827 10.527 1.486 10.751 1.053 L 11.271 0.058 L 12.05 0.058 L 10.251 3.41 L 10.07 3.41 Z M 13.584 3.359 L 12.87 3.359 L 12.87 0.055 L 13.584 0.055 Z M 14.804 3.239 L 14.726 3.21 L 14.726 2.52 L 14.836 2.568 C 15.146 2.698 15.536 2.786 15.86 2.786 C 16.082 2.786 16.26 2.753 16.381 2.695 C 16.478 2.644 16.535 2.579 16.535 2.488 C 16.535 2.386 16.495 2.31 16.395 2.241 C 16.278 2.157 16.085 2.085 15.793 1.998 C 15.029 1.776 14.697 1.496 14.697 0.959 C 14.697 0.375 15.193 0 16.028 0 C 16.363 0 16.724 0.062 16.984 0.168 L 17.034 0.186 L 17.034 0.857 L 16.924 0.807 C 16.648 0.688 16.35 0.626 16.049 0.625 C 15.839 0.625 15.668 0.655 15.55 0.719 C 15.454 0.77 15.396 0.843 15.396 0.937 C 15.396 1.028 15.436 1.101 15.532 1.173 C 15.65 1.261 15.839 1.34 16.128 1.428 C 16.884 1.656 17.234 1.925 17.234 2.451 C 17.234 3.051 16.742 3.414 15.882 3.414 C 15.514 3.414 15.104 3.344 14.801 3.236 Z M 20.089 0 C 21.273 0 22.076 0.698 22.076 1.71 C 22.076 2.724 21.27 3.421 20.089 3.421 C 18.908 3.421 18.101 2.724 18.101 1.711 C 18.101 0.698 18.907 0.001 20.088 0.001 Z M 20.089 2.771 C 20.834 2.771 21.352 2.346 21.352 1.711 C 21.352 1.075 20.834 0.647 20.088 0.647 C 19.343 0.647 18.818 1.072 18.818 1.711 C 18.818 2.35 19.339 2.771 20.088 2.771 Z M 24.499 0.058 C 25.373 0.058 25.908 0.454 25.908 1.13 C 25.908 1.573 25.64 1.91 25.188 2.067 L 26.043 3.363 L 25.255 3.363 L 24.505 2.183 L 23.906 2.183 L 23.906 3.363 L 23.2 3.363 L 23.2 0.059 L 24.499 0.059 Z M 23.906 0.665 L 23.906 1.598 L 24.527 1.598 C 24.93 1.598 25.194 1.438 25.194 1.13 C 25.194 0.821 24.924 0.665 24.502 0.665 Z M 27.325 0.091 L 28.263 1.435 L 29.23 0.058 L 30.047 0.058 L 28.62 2.074 L 28.62 3.363 L 27.906 3.363 L 27.906 2.073 L 26.479 0.059 L 27.296 0.059 L 27.321 0.091 Z" fill="rgb(142, 140, 153)" height="3.421000000000001px" id="P22Fbj16y" transform="translate(42 14.5)" width="30.047000091552746px"/><path d="M 2.034 14.412 L 9.998 14.325 L 11.532 11.558 L 13.58 15.168 L 1.602 15.168 L 1.032 16.17 L 15.285 16.17 L 12.092 10.541 L 12.549 9.717 L 16.673 16.987 L 0.571 16.987 L 0 17.989 L 18.386 17.989 L 13.116 8.7 L 13.559 7.902 L 19.285 18 L 20.42 18 L 10.212 0 Z M 10.212 2.004 L 12.984 6.896 L 12.542 7.695 L 10.305 3.755 L 4.799 13.381 L 3.75 13.392 Z M 10.305 5.752 L 11.981 8.708 L 11.525 9.532 L 10.319 7.408 L 7.139 13.352 L 5.951 13.367 Z M 10.347 9.459 L 10.965 10.545 L 9.423 13.323 L 8.271 13.337 Z" fill="url(%23vKxq0SU4w-1921182794-linear-gradient)" height="18px" id="vKxq0SU4w" width="20.42px"/><path d="M 0 1.002 L 0.57 0 L 16.677 0 L 18.387 1.003 L 0 1.003 Z" fill="url(%23qyqFJaVjA-1921182794-linear-gradient)" height="1.0030000000000001px" id="qyqFJaVjA" transform="translate(0 17)" width="18.387px"/><path d="M 0 1.006 L 0.567 0 L 12.545 0 L 14.254 1.006 Z" fill="url(%23KBptSRBQO-1921182794-linear-gradient)" height="1.0060000000000002px" id="KBptSRBQO" transform="translate(1 15)" width="14.254000000000005px"/><path d="M 0.578 8.79 L 4.906 1.02 L 4.325 0 L 0 7.792 Z" fill="url(%23Kgw6PgukY-1921182794-linear-gradient)" height="8.79px" id="Kgw6PgukY" transform="translate(9.5 5.5)" width="4.906000000000006px"/></g></svg>)

The Aligned Perspective

Evaluate your decision to sell or rent by analyzing true monthly cash flow, tax implications, and how the property fits your overall financial goals.

Chief of Staff

,

Key Takeaways:

Evaluate your decision to sell or rent by analyzing true monthly cash flow, tax implications, and how the property fits your overall financial goals.

Market conditions, risk tolerance, and lifestyle preferences play a crucial role in determining whether keeping or selling your home is the best strategy.

Consulting a vetted fiduciary advisor can help you model complex tradeoffs and make a confident, informed choice tailored to your unique circumstances.

Many homeowners relocating wonder: Should I sell my house or rent it out? The right choice depends on three factors: monthly cash flow after all costs, tax outcomes, and how the property fits your lifestyle goals. A vetted fiduciary advisor can help you model these tradeoffs alongside your complete financial picture. Explore strategic insights at Datalign Advisory to support your financial decisions.

Step-By-Step Framework: Run The Numbers Before You Decide

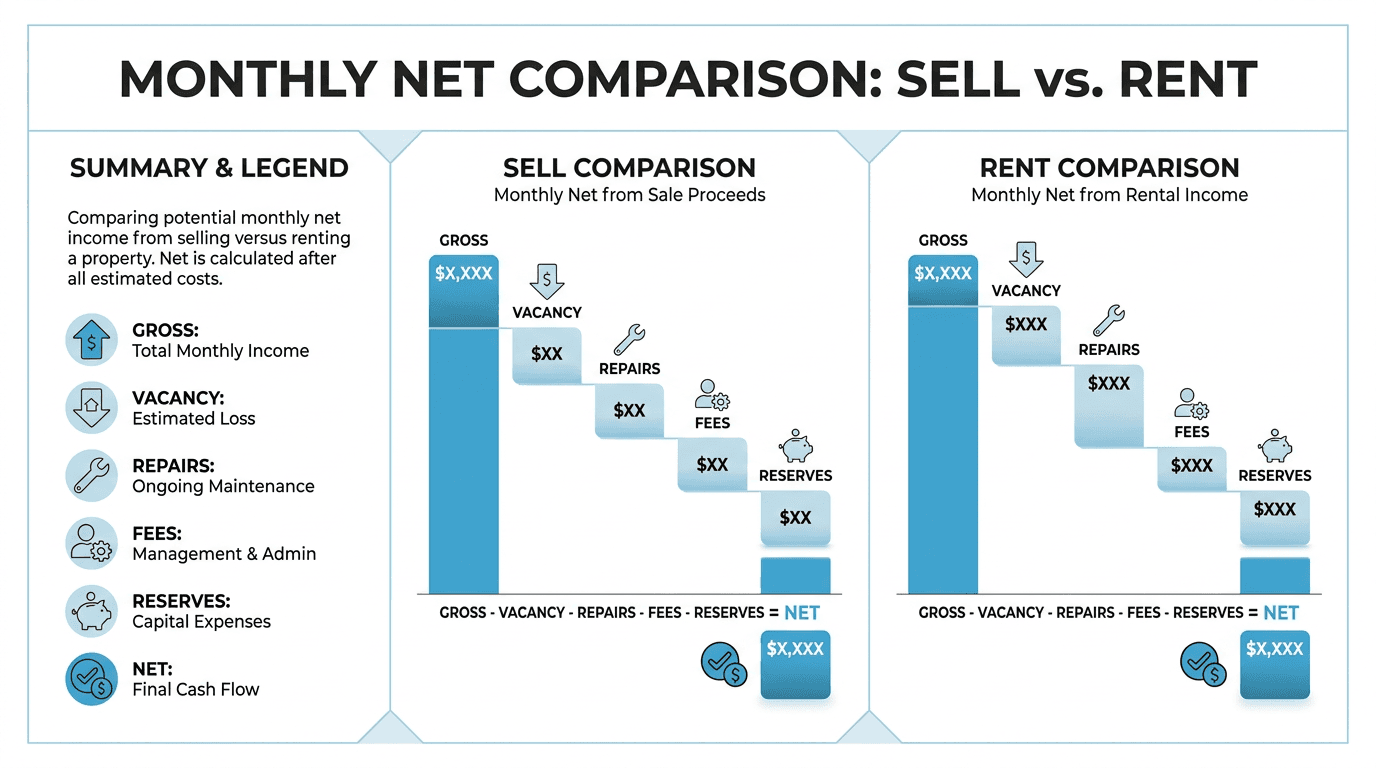

Understanding the financial pros and cons of keeping your house as a rental versus selling starts with honest math. Look beyond emotional attachment and focus on three concrete filters: true monthly cash flow, tax consequences, and how your equity serves your bigger goals.

Cash Flow Reality Check

Calculate realistic monthly rent, then subtract mortgage payments, property taxes, insurance, maintenance reserves, vacancy allowances, and management fees. Stress test your numbers using a vacancy rates data baseline of 40 days per year. If the result shows less than a $200 monthly cushion, selling might preserve your financial stability. For instance, if you expect $2,500 monthly rent but have $2,200 in total expenses, that $300 margin disappears quickly with one repair.

Tax Impact Analysis

Selling your primary residence can qualify for up to $250,000 (single) or $500,000 (married) in capital gains exclusion if you meet the ownership and use tests. Converting to a rental property means losing this exclusion and facing depreciation recapture when you eventually sell, but gaining annual depreciation deductions.

Equity Strategy Assessment

Compare keeping equity tied up in a rental property versus unlocking it through a sale. Selling provides immediate liquidity for debt payoff, investment diversification, or a down payment on your next home. Renting preserves potential appreciation but limits your financial flexibility and puts more of your wealth in one property.

Market, Risk, And Lifestyle Factors That Tip The Scale

Your local market and personal circumstances add important context to the financial picture. Several factors to consider when choosing to sell or rent your house involve your local market conditions, personal risk tolerance, and how property management fits your life. These practical elements often provide the clarity you need when the financial analysis shows similar outcomes.

Evaluate your local market trajectory - Supply-constrained neighborhoods with rising rents favor rental income growth, while slower-growth areas or communities with strict HOA rental restrictions make selling the safer choice.

Test your financial resilience - If a 37 percent rent drop or an unexpected $3,000 repair would strain your budget, prioritize the liquidity and simplicity that comes with selling rather than risking financial stress.

Consider your geographic flexibility needs - Renting preserves the option to move back if life changes, but selling eliminates ongoing maintenance obligations and gives you complete freedom to relocate without property management concerns.

Assess your tolerance for landlord duties - Property management calls, tenant screening, and repair coordination require time and emotional energy that selling eliminates, allowing you to focus on other financial goals without distraction.

Factor in your investment diversification - Keeping rental property concentrates wealth in one asset and location, while selling allows you to spread risk across different investments and geographic markets.

Make A Confident Move: Align The Decision With Your Goals

Start by listing realistic rental income, then subtract mortgage payments, taxes, insurance, maintenance, and management fees. Run a 12-month cash flow projection and stress test with roughly one month of vacancy per year to see if the numbers work.

If your analysis reveals close margins, consider consulting a fiduciary advisor who can model tax implications, opportunity costs, and how each option aligns with your wealth-building goals. You can make the right decision by assessing your risk capacity and timeline.

If you want to decide to sell or rent for long-term goals with confidence, explore the strategic insights and guidance available through Datalign Advisory's Educational Resources. For a deeper analysis on this specific decision, review our comprehensive guide on whether to sell your house or rent it out. As an SEC-registered platform, Datalign Advisory can connect you with a rigorously vetted, fiduciary advisor who understands your unique circumstances and values.

FAQs: Renting Versus Selling, Answered Clearly

Homeowners often underestimate hidden costs or miss tax implications that can shift the math entirely. These answers address the financial details that help you decide if renting or selling your home better serves your long-term goals.

What costs do owners commonly forget when estimating rental cash flow?

Property management fees, vacancy allowances, and repair reserves often get overlooked. Insurance costs typically increase for rental properties. Don't forget about advertising costs, tenant screening fees, and potential legal expenses. IRS guidance details deductible rental expenses that impact your true cash flow.

How do capital gains rules and depreciation recapture work if I convert my primary home to a rental?

Converting to rental use starts a clock that can limit your future capital gains exclusion eligibility. Any depreciation claimed reduces your cost basis and gets recaptured as ordinary income when you sell. IRS guidance explains these complex rules, though a qualified tax professional can model your specific situation.

How much emergency reserve should I hold if I keep the property as a rental?

Plan for 3-6 months of mortgage payments plus $3,000-$5,000 for major repairs. This can help cover appliance failures, HVAC issues, or unexpected maintenance needs. Your reserve requirements depend on the property's age and your comfort level with handling multiple expenses simultaneously.

Can I self-manage to save money, and when is a property manager worth the fee?

Self-management works if you live nearby, have time for tenant calls, and understand landlord-tenant laws. Professional management becomes worthwhile when you value your time, live far away, or lack tenant screening experience. The management fee often pays for itself by reducing vacancy and tenant turnover.

What timeline should I use for a vacancy and repair stress test?

Budget for 40 days of vacancy per year as a baseline stress test. This accounts for tenant turnover, seasonal rental patterns, and time needed for maintenance between tenants. Competitive markets typically see shorter vacancies; unique properties may take longer to rent.