"/><stop offset="1" stop-color="rgb(3, 73, 122)"/></linearGradient><linearGradient id="qyqFJaVjA-1921182794-linear-gradient" x1="0" x2="1" y1="0.5558218829289385" y2="0.4441781170710614"><stop offset="0" stop-color="rgb(29, 170, 88)"/><stop offset="1" stop-color="rgb(0, 143, 203)"/></linearGradient><linearGradient id="KBptSRBQO-1921182794-linear-gradient" x1="0" x2="1" y1="0.5556785500517466" y2="0.44432144994825334"><stop offset="0" stop-color="rgb(29, 170, 88)"/><stop offset="1" stop-color="rgb(0, 143, 203)"/></linearGradient><linearGradient id="Kgw6PgukY-1921182794-linear-gradient" x1="0.2117440484028747" x2="0.7882559515971252" y1="1" y2="5.551115123125783e-17"><stop offset="0" stop-color="rgb(0, 143, 203)"/><stop offset="1" stop-color="rgb(255, 255, 255)"/></linearGradient></defs><g d="M 25.388 5.232 L 25.388 10.89 L 26.819 10.89 C 29.017 10.89 30.33 9.837 30.33 8.061 C 30.33 6.285 28.996 5.232 26.766 5.232 L 25.387 5.232 Z M 24 12.008 L 24 4.118 L 26.79 4.118 C 29.895 4.118 31.746 5.599 31.746 8.065 C 31.746 10.53 29.916 12.012 26.844 12.012 L 24 12.012 Z M 38.74 9.415 C 38.233 8.438 37.652 7.265 37.166 6.248 C 36.665 7.317 36.137 8.373 35.582 9.415 Z M 37.113 4 L 37.22 4 L 41.53 12.015 L 40.064 12.015 L 39.179 10.413 L 35.129 10.413 L 34.266 12.015 L 32.799 12.015 L 37.109 4 Z M 45.954 5.232 L 45.954 12.008 L 44.567 12.008 L 44.567 5.232 L 41.809 5.232 L 41.809 4.118 L 48.714 4.118 L 48.714 5.232 L 45.955 5.232 Z M 54.927 9.415 C 54.421 8.438 53.84 7.265 53.354 6.248 C 52.853 7.317 52.324 8.373 51.77 9.415 L 54.928 9.415 Z M 53.302 4 L 53.409 4 L 57.719 12.015 L 56.256 12.015 L 55.371 10.413 L 51.321 10.413 L 50.458 12.015 L 48.992 12.015 Z M 59.88 12.008 L 59.88 4.114 L 61.268 4.114 L 61.268 10.89 L 65.158 10.89 L 65.158 12.008 Z M 68.892 4.5 L 67.5 4.5 L 67.5 12.39 L 68.892 12.39 Z M 76.924 12.177 C 73.994 12.177 72 10.522 72 8.089 C 72 5.656 74.002 4 76.935 4 C 78.326 4 79.208 4.305 79.779 4.57 L 79.779 5.808 C 78.894 5.415 77.935 5.214 76.967 5.217 C 74.844 5.217 73.403 6.379 73.403 8.089 C 73.403 9.799 74.826 10.972 76.924 10.972 C 77.495 10.972 78.216 10.874 78.658 10.732 L 78.658 8.408 L 79.993 8.408 L 79.993 11.578 C 79.218 11.942 77.97 12.181 76.924 12.181 M 85.16 7.698 C 84.792 7.368 84.385 7.03 84.157 6.808 C 84.157 7.106 84.167 7.586 84.167 7.905 L 84.167 12.038 L 82.791 12.038 L 82.791 4.024 L 82.888 4.024 L 87.844 8.475 L 88.836 9.376 C 88.825 9.071 88.825 8.664 88.825 8.279 L 88.825 4.147 L 90.201 4.147 L 90.201 12.161 L 90.116 12.161 L 85.159 7.698 Z M 42 17.859 L 43.799 14.508 L 43.941 14.508 L 45.743 17.859 L 44.98 17.859 L 44.627 17.224 L 43.107 17.224 L 42.764 17.859 Z M 44.366 16.661 C 44.198 16.331 44.034 16 43.874 15.666 C 43.72 15.993 43.542 16.346 43.378 16.661 Z M 47.799 14.555 C 49.09 14.555 49.85 15.18 49.85 16.207 C 49.85 17.235 49.097 17.859 47.82 17.859 L 46.607 17.859 L 46.607 14.555 Z M 47.32 15.161 L 47.32 17.249 L 47.81 17.249 C 48.63 17.249 49.13 16.868 49.13 16.204 C 49.13 15.539 48.623 15.158 47.791 15.158 L 47.321 15.158 L 47.321 15.161 Z M 52.07 17.907 L 52.087 17.874 L 50.307 14.554 L 51.085 14.554 L 51.795 15.913 C 51.941 16.2 52.059 16.425 52.177 16.672 C 52.341 16.327 52.527 15.986 52.751 15.553 L 53.271 14.558 L 54.05 14.558 L 52.251 17.91 L 52.07 17.91 Z M 55.584 17.859 L 54.87 17.859 L 54.87 14.555 L 55.584 14.555 Z M 56.804 17.739 L 56.726 17.71 L 56.726 17.02 L 56.836 17.068 C 57.146 17.198 57.536 17.286 57.86 17.286 C 58.082 17.286 58.26 17.253 58.381 17.195 C 58.478 17.144 58.535 17.079 58.535 16.988 C 58.535 16.886 58.495 16.81 58.395 16.741 C 58.278 16.657 58.085 16.585 57.793 16.498 C 57.029 16.276 56.697 15.996 56.697 15.459 C 56.697 14.875 57.193 14.5 58.028 14.5 C 58.363 14.5 58.724 14.562 58.984 14.668 L 59.034 14.686 L 59.034 15.357 L 58.924 15.307 C 58.648 15.188 58.35 15.126 58.049 15.125 C 57.839 15.125 57.668 15.155 57.55 15.219 C 57.454 15.27 57.396 15.343 57.396 15.437 C 57.396 15.528 57.436 15.601 57.532 15.673 C 57.65 15.761 57.839 15.84 58.128 15.928 C 58.884 16.156 59.234 16.425 59.234 16.951 C 59.234 17.551 58.742 17.914 57.882 17.914 C 57.514 17.914 57.104 17.844 56.801 17.736 Z M 62.089 14.5 C 63.273 14.5 64.076 15.198 64.076 16.21 C 64.076 17.224 63.27 17.921 62.089 17.921 C 60.908 17.921 60.101 17.224 60.101 16.211 C 60.101 15.198 60.907 14.501 62.088 14.501 Z M 62.089 17.271 C 62.834 17.271 63.352 16.846 63.352 16.211 C 63.352 15.575 62.834 15.147 62.088 15.147 C 61.343 15.147 60.818 15.572 60.818 16.211 C 60.818 16.85 61.339 17.271 62.088 17.271 Z M 66.499 14.558 C 67.373 14.558 67.908 14.954 67.908 15.63 C 67.908 16.073 67.64 16.41 67.188 16.567 L 68.043 17.863 L 67.255 17.863 L 66.505 16.683 L 65.906 16.683 L 65.906 17.863 L 65.2 17.863 L 65.2 14.559 L 66.499 14.559 Z M 65.906 15.165 L 65.906 16.098 L 66.527 16.098 C 66.93 16.098 67.194 15.938 67.194 15.63 C 67.194 15.321 66.924 15.165 66.502 15.165 Z M 69.325 14.591 L 70.263 15.935 L 71.23 14.558 L 72.047 14.558 L 70.62 16.574 L 70.62 17.863 L 69.906 17.863 L 69.906 16.573 L 68.479 14.559 L 69.296 14.559 L 69.321 14.591 Z M 2.034 14.412 L 9.998 14.325 L 11.532 11.558 L 13.58 15.168 L 1.602 15.168 L 1.032 16.17 L 15.285 16.17 L 12.092 10.541 L 12.549 9.717 L 16.673 16.987 L 0.571 16.987 L 0 17.989 L 18.386 17.989 L 13.116 8.7 L 13.559 7.902 L 19.285 18 L 20.42 18 L 10.212 0 Z M 10.212 2.004 L 12.984 6.896 L 12.542 7.695 L 10.305 3.755 L 4.799 13.381 L 3.75 13.392 Z M 10.305 5.752 L 11.981 8.708 L 11.525 9.532 L 10.319 7.408 L 7.139 13.352 L 5.951 13.367 Z M 10.347 9.459 L 10.965 10.545 L 9.423 13.323 L 8.271 13.337 Z M 0 18.002 L 0.57 17 L 16.677 17 L 18.387 18.003 L 0 18.003 Z M 1 16.006 L 1.567 15 L 13.545 15 L 15.254 16.006 Z M 10.078 14.29 L 14.406 6.52 L 13.825 5.5 L 9.5 13.292 Z" fill="transparent" height="18.003px" id="K_8etyHP8" width="90.20100036621093px"><path d="M 1.388 1.232 L 1.388 6.89 L 2.819 6.89 C 5.017 6.89 6.33 5.837 6.33 4.061 C 6.33 2.285 4.996 1.232 2.766 1.232 L 1.387 1.232 Z M 0 8.008 L 0 0.118 L 2.79 0.118 C 5.895 0.118 7.746 1.599 7.746 4.065 C 7.746 6.53 5.916 8.012 2.844 8.012 L 0 8.012 Z M 14.74 5.415 C 14.233 4.438 13.652 3.265 13.166 2.248 C 12.665 3.317 12.137 4.373 11.582 5.415 Z M 13.113 0 L 13.22 0 L 17.53 8.015 L 16.064 8.015 L 15.179 6.413 L 11.129 6.413 L 10.266 8.015 L 8.799 8.015 L 13.109 0 Z M 21.954 1.232 L 21.954 8.008 L 20.567 8.008 L 20.567 1.232 L 17.809 1.232 L 17.809 0.118 L 24.714 0.118 L 24.714 1.232 L 21.955 1.232 Z M 30.927 5.415 C 30.421 4.438 29.84 3.265 29.354 2.248 C 28.853 3.317 28.324 4.373 27.77 5.415 L 30.928 5.415 Z M 29.302 0 L 29.409 0 L 33.719 8.015 L 32.256 8.015 L 31.371 6.413 L 27.321 6.413 L 26.458 8.015 L 24.992 8.015 Z M 35.88 8.008 L 35.88 0.114 L 37.268 0.114 L 37.268 6.89 L 41.158 6.89 L 41.158 8.008 Z" fill="rgb(132, 130, 142)" height="8.015px" id="jAL5eYCXu" transform="translate(24 4)" width="41.15800106811523px"/><path d="M 1.392 0 L 0 0 L 0 7.89 L 1.392 7.89 Z" fill="rgb(132, 130, 142)" height="7.890000000000001px" id="u8cKeOXNI" transform="translate(67.5 4.5)" width="1.391999999999996px"/><path d="M 4.924 8.177 C 1.994 8.177 0 6.522 0 4.089 C 0 1.656 2.002 0 4.935 0 C 6.326 0 7.208 0.305 7.779 0.57 L 7.779 1.808 C 6.894 1.415 5.935 1.214 4.967 1.217 C 2.844 1.217 1.403 2.379 1.403 4.089 C 1.403 5.799 2.826 6.972 4.924 6.972 C 5.495 6.972 6.216 6.874 6.658 6.732 L 6.658 4.408 L 7.993 4.408 L 7.993 7.578 C 7.218 7.942 5.97 8.181 4.924 8.181 M 13.16 3.698 C 12.792 3.368 12.385 3.03 12.157 2.808 C 12.157 3.106 12.167 3.586 12.167 3.905 L 12.167 8.038 L 10.791 8.038 L 10.791 0.024 L 10.888 0.024 L 15.844 4.475 L 16.836 5.376 C 16.825 5.071 16.825 4.664 16.825 4.279 L 16.825 0.147 L 18.201 0.147 L 18.201 8.161 L 18.116 8.161 L 13.159 3.698 Z" fill="rgb(132, 130, 142)" height="8.181px" id="kN7yl8Gfy" transform="translate(72 4)" width="18.201000366210934px"/><path d="M 0 3.359 L 1.799 0.008 L 1.941 0.008 L 3.743 3.359 L 2.98 3.359 L 2.627 2.724 L 1.107 2.724 L 0.764 3.359 Z M 2.366 2.161 C 2.198 1.831 2.034 1.5 1.874 1.166 C 1.72 1.493 1.542 1.846 1.378 2.161 Z M 5.799 0.055 C 7.09 0.055 7.85 0.68 7.85 1.707 C 7.85 2.735 7.097 3.359 5.82 3.359 L 4.607 3.359 L 4.607 0.055 Z M 5.32 0.661 L 5.32 2.749 L 5.81 2.749 C 6.63 2.749 7.13 2.368 7.13 1.704 C 7.13 1.039 6.623 0.658 5.791 0.658 L 5.321 0.658 L 5.321 0.661 Z M 10.07 3.407 L 10.087 3.374 L 8.307 0.054 L 9.085 0.054 L 9.795 1.413 C 9.941 1.7 10.059 1.925 10.177 2.172 C 10.341 1.827 10.527 1.486 10.751 1.053 L 11.271 0.058 L 12.05 0.058 L 10.251 3.41 L 10.07 3.41 Z M 13.584 3.359 L 12.87 3.359 L 12.87 0.055 L 13.584 0.055 Z M 14.804 3.239 L 14.726 3.21 L 14.726 2.52 L 14.836 2.568 C 15.146 2.698 15.536 2.786 15.86 2.786 C 16.082 2.786 16.26 2.753 16.381 2.695 C 16.478 2.644 16.535 2.579 16.535 2.488 C 16.535 2.386 16.495 2.31 16.395 2.241 C 16.278 2.157 16.085 2.085 15.793 1.998 C 15.029 1.776 14.697 1.496 14.697 0.959 C 14.697 0.375 15.193 0 16.028 0 C 16.363 0 16.724 0.062 16.984 0.168 L 17.034 0.186 L 17.034 0.857 L 16.924 0.807 C 16.648 0.688 16.35 0.626 16.049 0.625 C 15.839 0.625 15.668 0.655 15.55 0.719 C 15.454 0.77 15.396 0.843 15.396 0.937 C 15.396 1.028 15.436 1.101 15.532 1.173 C 15.65 1.261 15.839 1.34 16.128 1.428 C 16.884 1.656 17.234 1.925 17.234 2.451 C 17.234 3.051 16.742 3.414 15.882 3.414 C 15.514 3.414 15.104 3.344 14.801 3.236 Z M 20.089 0 C 21.273 0 22.076 0.698 22.076 1.71 C 22.076 2.724 21.27 3.421 20.089 3.421 C 18.908 3.421 18.101 2.724 18.101 1.711 C 18.101 0.698 18.907 0.001 20.088 0.001 Z M 20.089 2.771 C 20.834 2.771 21.352 2.346 21.352 1.711 C 21.352 1.075 20.834 0.647 20.088 0.647 C 19.343 0.647 18.818 1.072 18.818 1.711 C 18.818 2.35 19.339 2.771 20.088 2.771 Z M 24.499 0.058 C 25.373 0.058 25.908 0.454 25.908 1.13 C 25.908 1.573 25.64 1.91 25.188 2.067 L 26.043 3.363 L 25.255 3.363 L 24.505 2.183 L 23.906 2.183 L 23.906 3.363 L 23.2 3.363 L 23.2 0.059 L 24.499 0.059 Z M 23.906 0.665 L 23.906 1.598 L 24.527 1.598 C 24.93 1.598 25.194 1.438 25.194 1.13 C 25.194 0.821 24.924 0.665 24.502 0.665 Z M 27.325 0.091 L 28.263 1.435 L 29.23 0.058 L 30.047 0.058 L 28.62 2.074 L 28.62 3.363 L 27.906 3.363 L 27.906 2.073 L 26.479 0.059 L 27.296 0.059 L 27.321 0.091 Z" fill="rgb(142, 140, 153)" height="3.421000000000001px" id="P22Fbj16y" transform="translate(42 14.5)" width="30.047000091552746px"/><path d="M 2.034 14.412 L 9.998 14.325 L 11.532 11.558 L 13.58 15.168 L 1.602 15.168 L 1.032 16.17 L 15.285 16.17 L 12.092 10.541 L 12.549 9.717 L 16.673 16.987 L 0.571 16.987 L 0 17.989 L 18.386 17.989 L 13.116 8.7 L 13.559 7.902 L 19.285 18 L 20.42 18 L 10.212 0 Z M 10.212 2.004 L 12.984 6.896 L 12.542 7.695 L 10.305 3.755 L 4.799 13.381 L 3.75 13.392 Z M 10.305 5.752 L 11.981 8.708 L 11.525 9.532 L 10.319 7.408 L 7.139 13.352 L 5.951 13.367 Z M 10.347 9.459 L 10.965 10.545 L 9.423 13.323 L 8.271 13.337 Z" fill="url(%23vKxq0SU4w-1921182794-linear-gradient)" height="18px" id="vKxq0SU4w" width="20.42px"/><path d="M 0 1.002 L 0.57 0 L 16.677 0 L 18.387 1.003 L 0 1.003 Z" fill="url(%23qyqFJaVjA-1921182794-linear-gradient)" height="1.0030000000000001px" id="qyqFJaVjA" transform="translate(0 17)" width="18.387px"/><path d="M 0 1.006 L 0.567 0 L 12.545 0 L 14.254 1.006 Z" fill="url(%23KBptSRBQO-1921182794-linear-gradient)" height="1.0060000000000002px" id="KBptSRBQO" transform="translate(1 15)" width="14.254000000000005px"/><path d="M 0.578 8.79 L 4.906 1.02 L 4.325 0 L 0 7.792 Z" fill="url(%23Kgw6PgukY-1921182794-linear-gradient)" height="8.79px" id="Kgw6PgukY" transform="translate(9.5 5.5)" width="4.906000000000006px"/></g></svg>)

The Aligned Perspective

Diversifying a concentrated stock position is essential for wealth preservation, and can be achieved through a combination of structured selling, charitable strategies, and advanced hedging tools to minimize taxes and risk.

Director of Growth

,

Key Takeaways:

Diversifying a concentrated stock position is essential for wealth preservation, and can be achieved through a combination of structured selling, charitable strategies, and advanced hedging tools to minimize taxes and risk.

A written, disciplined diversification plan—coordinated with a fiduciary advisor—helps ensure effective execution, tax optimization, and alignment with your long-term financial and philanthropic goals.

Leveraging professional guidance from a vetted fiduciary advisor is critical for navigating complex strategies, regulatory requirements, and integrating tax, estate, and investment planning.

Stock concentration builds fortunes, but it can destroy them just as quickly. Without a plan, you risk losing decades of wealth to a single stock's decline. An effective approach to diversifying a concentrated stock position combines gradual selling, charitable tools, and protective strategies that reduce taxes while maintaining control. Datalign Advisory can connect you with a vetted fiduciary advisor to design your personalized diversification plan.

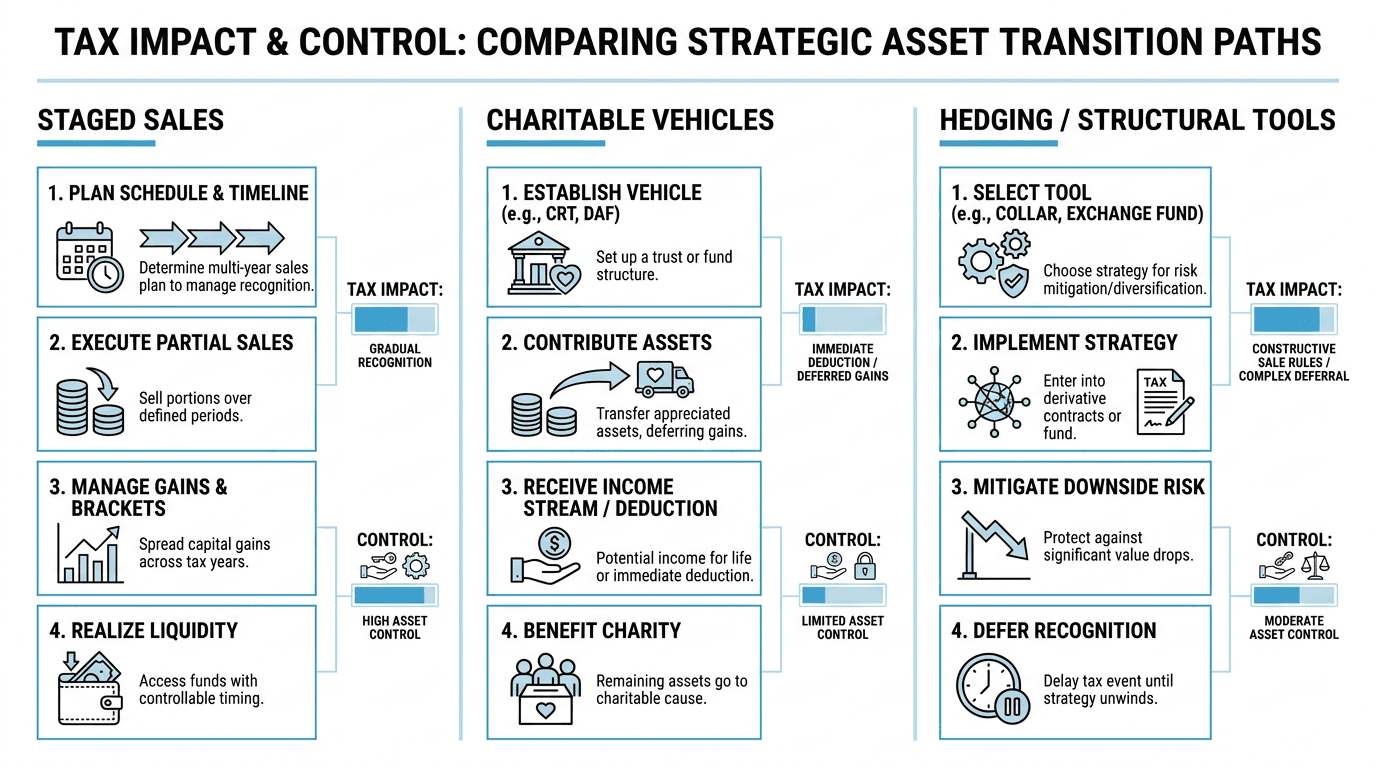

Tax-Savvy Ways to Reduce Single-Stock Risk

The challenge of how to diversify a concentrated stock position without triggering large capital gains taxes requires a coordinated approach, such as spreading recognition across multiple years while maximizing available offsets. Effective tax planning involves layering multiple strategies to minimize your overall tax burden while reducing concentration risk.

Establish a Rule 10b5-1 selling plan to pre-commit to staged sales across multiple tax years, allowing you to harvest gains gradually while pairing sales with tax-loss harvesting and charitable contributions to offset recognition.

Contribute appreciated shares to a donor-advised fund for an immediate charitable deduction while avoiding capital gains, or establish a charitable remainder trust to generate lifetime income while deferring tax recognition on the contributed shares.

Consider exchange funds or prepaid variable forwards for sophisticated hedging strategies. Exchange funds allow you to swap your concentrated position into a diversified basket of similar stocks, while prepaid variable forwards let you lock in current value, raise liquidity, and defer capital gains recognition for several years. These complex instruments require careful professional guidance.

Coordinate timing with comprehensive tax planning to execute tranches during lower-income years, maximize charitable deduction benefits, and layer multiple strategies to create the most tax-efficient diversification path for your specific situation.

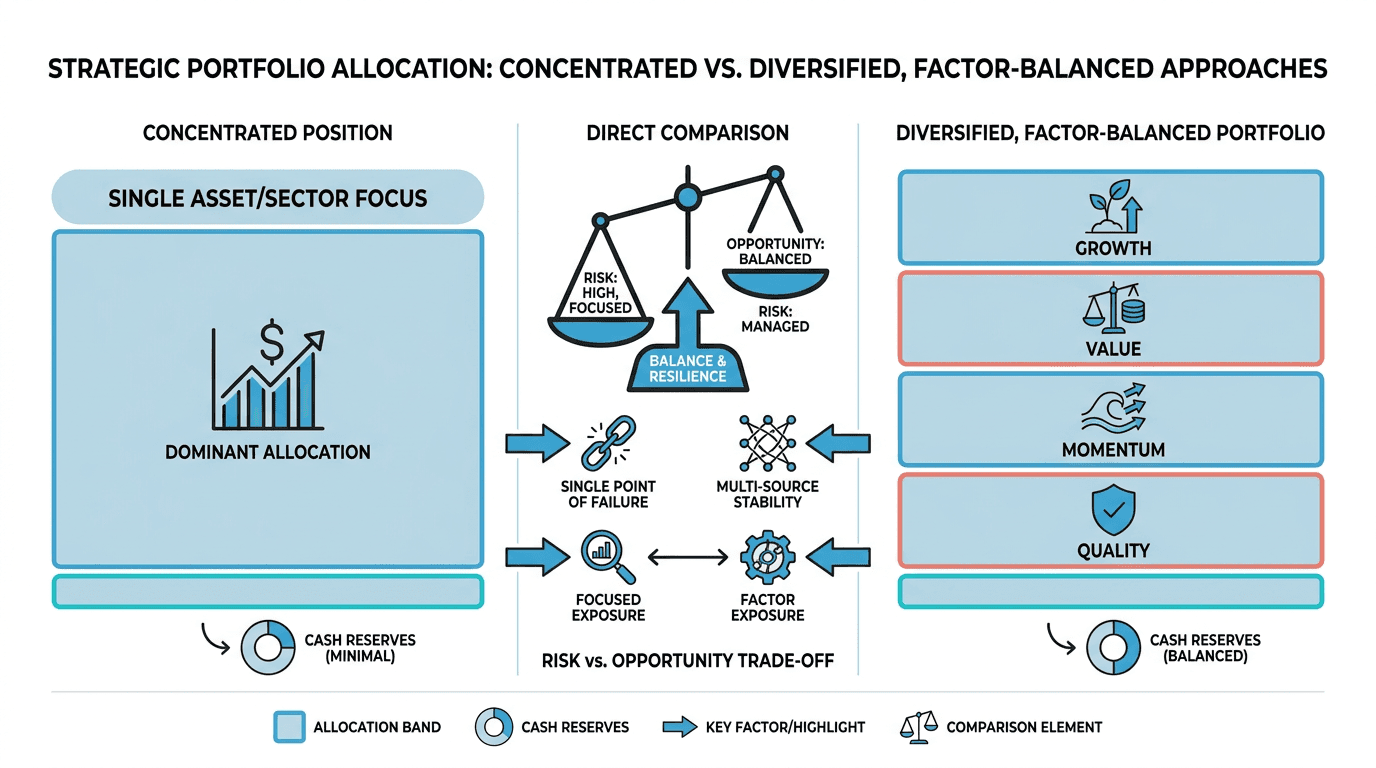

Designing the Portfolio After Diversification

Once you've reduced concentration risk, the next phase involves building a resilient portfolio around your remaining position. Smart approaches to reduce risk from holding too much of one stock include setting clear allocation targets, diversifying across asset classes and regions, and optimizing tax location to preserve wealth across generations.

Set Clear Allocation Bands and Rebalancing Rules

Target your legacy stock position down to 33 percent of total assets, then to 22 percent over 18 to 24 months. Establish specific price thresholds and calendar triggers for rebalancing. Decide in advance when you'll sell more shares to prevent emotional decision-making during market volatility.

Rebuild for Broad Market Exposure and Stability

Focus on broad stock market exposure plus areas you're missing, like international stocks, smaller companies, and value-oriented investments. Add bonds and other income sources for stability and steady cash flow. Keep three to six months of living expenses in cash to avoid forced selling during downturns.

Optimize Tax Location and Estate Integration

Place income-generating assets in retirement accounts while keeping highly appreciated stocks in taxable accounts for step-up basis benefits. Coordinate with estate planning through charitable trusts and systematic gifting. Plan for a greater than 90 percent confidence level in funding your lifetime and legacy goals through careful account management.

Next Steps: Create a Written Diversification Plan

A successful diversified concentrated stock position plan requires documented parameters and professional execution. Write down your 22 to 33-month timeline with specific tranche sizes, tax thresholds, and charitable allocation targets.

To execute this effectively, professional guidance transforms planning into implementation. A qualified fiduciary advisor can coordinate your tax planning, estate documents, and execution timing while maintaining fiduciary standards.

Datalign Advisory can connect you in minutes with a vetted, SEC-registered fiduciary advisor who specializes in concentrated position strategies. The free platform uses AI-enhanced matching to align you with an advisor who understands your goals and preferences. Before meeting, review key questions to ensure your advisor can document and execute your specific diversification timeline.

Get matched with a trusted advisor today to build your written plan and start reducing concentration risk.

FAQ: Managing a Concentrated Stock Position With a Fiduciary

Managing a concentrated stock position requires coordinating sale timing, tax strategies, charitable giving, and estate planning around one large holding. Fiduciary advisors bring legal protections that matter when balancing these competing priorities without conflicts that could compromise your outcomes.

How can a fiduciary advisor coordinate 10b5-1 plans, charitable vehicles, and estate documents without conflicts of interest?

Fiduciary advisors must act in your best interest and disclose any conflicts in writing. They coordinate timing across strategies because they're legally bound to seek ways to optimize your objective outcomes, not generate commissions or unnecessary fees. SEC regulations require waiting periods and written certifications for trading plans, ensuring independent decision-making.

What are practical triggers for executing tranches during diversification?

Common triggers include price bands (for example, sell 25% if the stock rises 20%), tax thresholds (harvest gains up to the 20% capital gains bracket), and calendar windows (quarterly reviews with annual limits). Market swings can also trigger faster sales when your stock moves much more than the overall market. The key is to document these rules in advance within your 10b5-1 plan with tax-aware timing.

When do exchange funds or prepaid variable forwards make sense versus simply selling and paying the tax?

Exchange funds work best when you can commit capital for seven years, and your tax rate exceeds 25%. Prepaid forwards make sense when you need cash now but want to delay paying taxes. For smaller positions or when you need flexibility, direct selling is often simpler and more cost-effective.

How do I verify an advisor can handle these complex strategies?

Ask specific questions about their experience with concentrated positions and request references from similar clients. Verify their fiduciary status through FINRA BrokerCheck or SEC IAPD databases. The right advisor should demonstrate familiarity with tax coordination, estate planning integration, and regulatory requirements for sophisticated strategies.

Disclaimer: This information is for educational purposes only and is not intended as, nor should it be relied upon as, individualized financial, investment, tax, or legal advice, and you should consult a qualified professional about your specific circumstances before making any financial decisions.